Central Bank Digital Currencies (CBDCs) could well be one of the most far-reaching advances of the 21st century. Taken to the extreme, these forms of digital payment could potentially void the need for traditional banks altogether while the technology underlying tokenized forms of CBDCs opens up boundless possibility for novel forms of economic policy.

China is the furthest along in its CBDC development roadmap and has already rolled out pilot tests in several major cities. Going by the official moniker of “DCEP” (“Digital Currency/Electronic Payment”), the country is expected to have a mass rollout right in time for the 2022 Winter Olympics in Beijing. China’s progress on this front, coupled with Facebook’s 2019 announcement of its own digital currency, Libra (now known as “Diem”), were two of the catalysts for the latter day “space race” to develop CBDCs. The BIS reports that 86% of Central banks are developing a digital currency and around 14% are in the process of rolling out pilot tests. Long a holdout, Jerome Powell also recently announced that the US Fed intends to publish a discussion paper on a digital dollar this summer.

The People’s Bank of China (“PBOC”) first initiated development on the DCEP in 2014 under the guidance of highly regarded governor, Zhou Xiaochuan. That China is the global leader in this space should come as no surprise, given that the country is already a leader in electronic payment systems. As China’s CBDC inches closer to launch, we take a look at key features of the DCEP’s design and the implications this could have for the wider political economy.

How Does the DCEP Work?

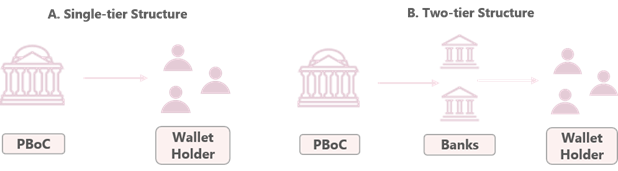

From a user perspective, the DCEP functions as a standard wallet or electronic payment app akin to Venmo or WeChat Pay. Screenshots of the app have emerged from pilot tests over social media and the below image is a snapshot of the China Construction Bank’s DCEP wallet app. The choice of delegating the wallet and distribution to banks speaks to the “two-tier” system the PBOC is employing, which will keep banks from being disintermediated.

Screenshots of the CCB’s Digital Yuan Wallet

It is worthwhile to peek under the hood, and examine the potential design choices available to Central banks in rolling out CBDCs. At the outset, it’s important to note that while Central banks digital currencies make use of cryptographic technologies, they are not employing “blockchain” technology in the strictest sense of the term. They are centrally-operated and eschew typical consensus protocols such as proof-of-work or proof-of-stake, for bespoke mechanisms. In the DCEP’s case there is a central entity maintaining the ledger referred to as a “registration center.”

Key Design Features of Central Bank Money

Apart from greater control, there are also sustainability and scalability considerations at play. The blockchain ecosystem at present is massively inefficient in regards to resource consumption, which limits its scalability. The Bitcoin network, the blockchain that supports the most well-known cryptocurrency, is only capable of processing a maximum of seven transactions per second. The Visa network, by contrast, typically supports approximately 1,700 transactions per second.

The Technology Behind China’s DCEP

How is DCEP different from existing cryptocurrencies? The digital yuan is not supported by a blockchain nor is it considered a cryptocurrency in the strictest sense. It is instead a digital token currency which relies on cryptography and some blockchain concepts, while lacking the decentralized ledger akin to a blockchain. This centrally-managed ledger instead retains the monetary controls traditional afforded to the governing Central bank. Additionally, given the vast computational power associated with blockchain-based cryptocurrencies, this is a natural outcome for a sovereign currency and a direction that other CBDCs will also take.

The PBOC intends to maintain three core departments: a “Registration Center” responsible for maintaining the centralized ledger of all currency activity, an “Authentication Center” responsible for verifying the identities of parties involved, and a “Big Data” Center responsible for data-mining DCEP transactions.

Core ‘Departments’ of China’s DCEP

The DCEP will also be usable without an active internet connection. DCEP money will be transferable via the use of NFC (near-field communication), which allows the for the communication of two electronic devices in close proximity similarly to electronic payment apps like Apple Pay and Samsung Pay. It will also be accompanied by a rollout of hardware wallets fully functional for operating offline, which will help expand DCEP adoption in rural and remote areas with lagging access to internet connectivity.

Tier-Based Based Provision of DCEP

As mentioned earlier, CBDCs present a significant threat to financial institutions. The decentralized nature of CBDC-based digital wallets eliminates the need for banking intermediaries. Theoretically, it would be possible for Central banks harness CBDCs to put themselves in the position of sole financial intermediary where they directly face the customer. However, while possible, it remains unlikely to occur. Central banks would need to scale their operations massively with customer service hotlines and compliance back office operations which are presently being quarterbacked by the private sector system. Additionally, given the entire global system of modern credit is backed by banking deposits, disintermediation of traditional financial institutions could destabilize the entire financial system.

For these reasons CBDCs rollouts are all but certain to go the way of a two-tiered system, where banks remain involved. This is exactly what the digital yuan has done. The PBOC will release DCEP to the banks, who in turn will enable customers to swap their existing cash balances for DCEP units. More critically, interest will only be earned on deposits once customers place digital currency with banks. The PBOC itself will not be responsible for interest rate transmission.

Options for CBDC Rollout Structure

This structure is what is referred to as a “two-tier” CBDC and will keep legacy banks relevant as they manage the operational logistics of the CBDC as well as develop and maintain their own digital wallet apps for the DCEP. Over the long-term, once the DCEP achieves widespread adoption, it is possible that banks and legacy financial institutions will become relegated to a role more akin to “plumbers” of the financial system. Meanwhile, policy functions like interest rate transmission could potentially migrate to the Central bank, with tokenization enabling a direct pass through.

This arrangement also implies that the DCEP may ultimately present little threat to AliPay and WeChat Pay as users of the two platforms may simply link their wallets to the DCEP to continue enjoying platform benefits and functionality.

Will the DCEP Employ Smart Contract Technology?

The PBOC has explicitly acknowledged that the DCEP incorporates smart contract technology. However, detailed plans for contract functionality are not known, and it is likely that regulators will hold back on significant smart contract integration given the nascency of the technology. However, the DCEP’s basic design does make smart contract programming a possibility, and the PBOC is likely researching and studying potential use cases.

Will the DCEP Be Account-Based or Token Based?

One of the design choices available to Central banks is to have a simple “account-based” system instead of tokenized money. Launching a cryptographic token is not essential to circulating a digital centralized currency and Central banks can achieve the same objective via traditional database technology. In the DCEP’s case, this is largely academic as the choice has already been made in favor of tokens. It is nonetheless a distinction that pops up in the literature and discourse around CBDCs. Global Central bank preferences also seem to be largely in favor of tokenized money, so account-based systems may simply end up being an academic strawman.

Wholesale or Retail CBDCs?

Some countries have mulled the possibility of a CBDC restricted to financial and institutional players, known as a “wholesale CBDC,” as opposed to a general purpose CBDC. China’s DCEP project is decidedly a general purpose CBDC. Thailand is an example of a country focused on wholesale CBDCs: the nation is currently solving for a wholesale CBDC which can be used for cross-border and domestic interbank payments. The consideration for doing so appears to be logistical so far, and it is likely that most the national CBDC projects will pivot towards including retail users. Hong Kong, for instance, recently committed to a retail CBDC after initially leaning towards wholesale CBDCs.

Why Is China Creating a Digital Currency?

In the age of cryptocurrency, CBDC development was inevitable. The DCEP will not only increase the speed and convenience of transactions but a fiat digitized currency will also open up new frontiers for business and the wider economic landscape.

Cross-Border Trade & Payments

One of the greatest pain points in payments right now is the convoluted system of cross-border payments, which apart from being slow and cumbersome, also penalize small value payments. This has led many to search for alternatives, and a good example is Nigerian overseas workers who have turned to Bitcoin as a quick, cost-effective way to remit money home. A CBDC would provide similar benefits, but without the associated price volatility.

Poignantly, the US-China trade war also brought to light the subject of monetary sanctions, in which US policymakers can potentially restrict dollar access for China via its leverage over SWIFT. The DCEP could provide a way to circumvent potential sanctions.

At this point, it is worth a small digression to understand a key question: how do current cross-border payment systems work? Cross-border payments are effectively coordinated by what is known as the “correspondent banking” system. A correspondent bank is a financial institution with operations in two or more countries which have agreements to provide services for each other. Imagine the following scenario. If you send money from Singapore to someone in Australia, you will first instruct your personal bank to send the money. Your bank will in turn notify its correspondent bank to wire money to its Australian counterpart. The correspondent bank branch in Australia will ultimately wire the money to the receiver’s personal bank.

Cross-Border Payment Flow

Digital Wallet Transfers

If you consider the flow above – it becomes clear why cross-border payments can be costly and time consuming. There are too many handshakes, and the cost of keeping the ball rolling means banks end up overcharging for small payments. Replacing this system with digital wallets would remove all middlemen. Instead of multiple entries managing multiple ledgers, via a bespoke messaging system – the token transfer would happen directly between end users.

Furthermore, the lynchpin of the correspondent banking system is the SWIFT messaging platform that undergirds the whole transfer process. While it is not a money transfer system and simply provides a safe channel for correspondent banks to receive secure instructions, restricted access to SWIFT is nonetheless one tool the US has in its financial arsenal against China. Digital wallet transfers would not require banks at all (or would certainly eschew SWIFT in the case of a strong two-tier system) and therefore greatly weaken one of the US’ strongest weapons.

A Boon to International RMB Usage

While the sanctions angle is headline-worthy, the simplicity and ease of DCEP can also provide a boost to RMB-denominated trade. RMB internationalization has been a consistent policy goal enshrined in multiple five-year plans. While the key barrier to internationalization remains macroeconomic constraints, there is considerable potential for tokenized money to reinvent the trade system.

Richard Turin articulates these possibilities in his book “Cashless: China’s Digital Currency Revolution.” He concludes that CBDCs could potentially give rise to a targeted system of trade incentives, such as preferential exchange rates depending on the country or product bought and sold, all enabled by tokenized cash. This could potentially be applied to capital controls to culminate in “programmed capital controls” which flick targeted cross-border flow on and off effortlessly. In a world looking to pivot away from China, a novel trade system micro-targeting and calibrating incentives as seamlessly as Big Tech companies could be a significant play. Naturally this is all in the realm of speculation but the technology behind digital money implies that this may be all but a long-term inevitability.

Financial Inclusion

Despite its progress towards digitalization, China remains home to the world’s largest unbanked population at approximately 225 million. Vast population segments like those in rural villages and the elderly are not vaunted target markets for banks largely due to the costs of last-mile delivery. DCEP wallets could go some way towards ameliorating this inefficiency by introducing electronic payment services in these areas. By design, a DCEP wallet rollout would not require rural villagers to suffer visits to remote bank branches or even have access to a bank account while still providing certain advantages of digital banking services. It would also be an easy low-cost platform for traditional banks through which to offer other value-added services to underrepresented segments.

Novel Forms of Monetary & Fiscal Policy

CBDCs can have profound implications for monetary policy and the wider macro-economic policy apparatus, and can have interest rates “embedded” in the token itself. In the present financial system, the Central bank influences market rates indirectly by way of its own lending rate to financial institutions, otherwise known as the Central bank discount rate. By programming rates into tokenized money, CBDCs can enable direct transmission. This could be combined with Big Data to isolate segments of the population; pensioners and elderly for instance could be provided with higher interest rates. As stimulus measures, CBDCs can also enable “helicopter drops” of money to targeted segments of the population or big-data powered universal basic income disbursements.

Still, this is all in the realm of enlightened speculation as the PBOC has not highlighted any specific monetary policy use cases for the DCEP. In fact, the DCEP has been slated to not pay any interest for now, and is specifically intended as a replacement for cash (M0) as opposed to banking deposits or time deposits (M1 and M2). Leaving interest rate disbursement to banks is also a key feature of the two-tier model. While likely an eventual development, this would occur well into the future as CBDCs would have to become widespread enough before they are deployed for monetary policy.

Auxiliary Benefits of a DCEP

Availability of Smart Contracts

It is possible for Central Banks to enable Smart Contract technology in CBDC design. Programmable money will enable a panoply of use cases and could potentially disintermediate many services by allowing for automated digital currency, fiat money, and shares exchange, while tokenized money could also be outfitted with conditionals such as “only x amount may be spent per day.” Smart contracts are still very much an emerging technology, and will not be a heavily advertised feature at the outset though potential use cases in the long-term are endless.

Superior Forensics & Tax Collection

The DCEP and other CBDCs will by design leave a comprehensive virtual audit trail of money usage, and can significantly bolster anti-money laundering and compliance efforts. Tax evasion could become significantly more difficult as well.

Big Data

Data is the 21st century’s digital gold, and the success of Big Tech has been built on the back of vast monopolies of data. China’s Alibaba for instance has access to payment data (via AliPay), consumer purchase data (via TMall and Taobao), as well as locational data via the AutoNavi app. These moats have only been available to the private sector, but CBDCs threaten to flip the script by providing governments with granular consumer transaction data. This data can be mined to study economic trends and consumer behavior to an unprecedented degree. As we have seen in the preceding section, this is an explicit policy goal for the PBOC, and the bank is already in the process of instituting a big data department for the DCEP.

Merchant & Interchange fee

Domestic payment systems like card acquiring networks (MasterCard, Visa, UnionPay), ATM connectivity networks, and other payment rails are notorious for charging consumers transactional fees. Even China’s merchant friendly Alipay and WeChat charge businesses access fees of ~0.6%. DCEP wallets by design will incur no such costs and will transfer significant value to small- and medium-sized businesses.

The Road Ahead

CBDCs continue to progress at a breakneck pace, and it is highly likely that this article will be outdated or at least superseded within a few months of publication. China is set to lead the way, which speaks to its tremendous capacity for looking forward. The rollout of DCEP and other CBDCs will bring significant reverberations across finance and industry, and, with the passage of time, perhaps even fundamental changes to our basic economic system.

Pingback: How China Leads in Blockchain Innovation for Business