In 2019, China’s trade accounted for 36% of its GDP, a steep decline from its peak of nearly 65% in 2006. The decrease is no coincidence — Beijing has had its heart set on stabilizing long-term growth by harnessing the power of domestic production and consumption as cemented in China’s ‘Made in China 2025’ policy. Despite shifting towards self-reliance, the transition will take time. Since the ‘reform and opening up’ era of the 1980s, China has established itself as a crucial exporter of both labor- and capital-intensive goods while progressing on its goals of poverty eradication and national growth.

Fast forward to today, where China’s key relationships with countries including the US, Australia, and EU, are all under fire. With China’s exporters at risk, Beijing has been quick to rebalance its economic interests and domestic policies via two trade agreements: the Regional Comprehensive Economic Partnership (RCEP) and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (TPP11). Once negotiated, the initiatives will span a large trade bloc of both current and new partners, thereby offering China an opportunity to bolster its trade influence and secure alternative countries with whom to conduct trade.

Current Trade Struggles Threaten Future Relationships

China has been re-evaluating its trade partnerships through the lens of what it considers to be within and outside the scope of economic collaboration. From geopolitical tensions to trade barriers, China’s pre-existing partnerships are collapsing quickly – particularly with the US, the EU, and Australia. Aside from the individual concerns that each country has about China, they all share collective grievances towards the country’s domestic policies. From Hong Kong’s new national security law to ‘unfair’ business practices, ideological differences between itself and many Western trading partners are significantly impairing China’s trade relationships.

Australia-China Trade

Over the past several months, China’s relationship with Australia has quickly spiraled out of control. China is Australia’s largest trading partner with trade between the two countries having grown by more than 20% between 2018 and 2019.

However, recent disputes have disrupted the trade relationship. The fallout could be seen earlier in 2020, when China suspended beef imports from 4 major meat processing plants in Queensland and New South Wales, followed by a tariff of 80.5% on Australian barley exports. Combined with increasingly weary diplomatic relations over recent years, the Sino-Australian relationship has deteriorated to a point where the potential for future trade growth is up in the air.

EU-China Trade

At the same time, China’s relationship with the EU has also been turbulent. These two powerhouses have been pivotal contributors to each others’ trade. The EU has been China’s largest trading partner until the collective ASEAN nations took the top spot in 2020. Meanwhile, China commands the spot of the EU’s second-largest trade partner after the US.

Regardless, the EU has historically been proactive in taking measures to protect itself from China-first policies, mainly through trade barriers and placing anti-dumping measures on Chinese products to protect its domestic market. More recently, the EU-China annual summit brought to surface irreconcilable differences between the two countries over issues like cybersecurity and human rights, topics that are currently being weighed in Brussels. Another point of contention that was discussed at the summit was the Hong Kong national security law, and shortly after, the EU took action by imposing new restrictions on the export of sensitive technologies to China in response.

US-China Trade

Finally, the US-China trade relationship has fallen apart over recent years. Trade tariffs, calls for a complete decoupling, and forced consulate closures on both sides all mark increasingly hostile relations between the two countries. Looking at the impact of the trade war, at least US$50 billion in tariffs in 2018 have escalated to US$550 billion in just two short years – wreaking economic havoc on both sides. Poignantly, the Phase One trade deal, a significant milestone in US-China trade relations, is becoming obsolete due to the pandemic – further shrouding the road ahead for the US-China trade relationship in uncertainty.

China’s Position

There are similar issues with numerous other trading partners as well. China has disputes or strained ties with 12 of its top 20 export destinations, be it border skirmishes with India or disputes over the South China Sea with the Philippines. In a simple numbers game, individual countries rely more on China and its supply chains than the other way around. Viewed collectively, however, this is not the case.

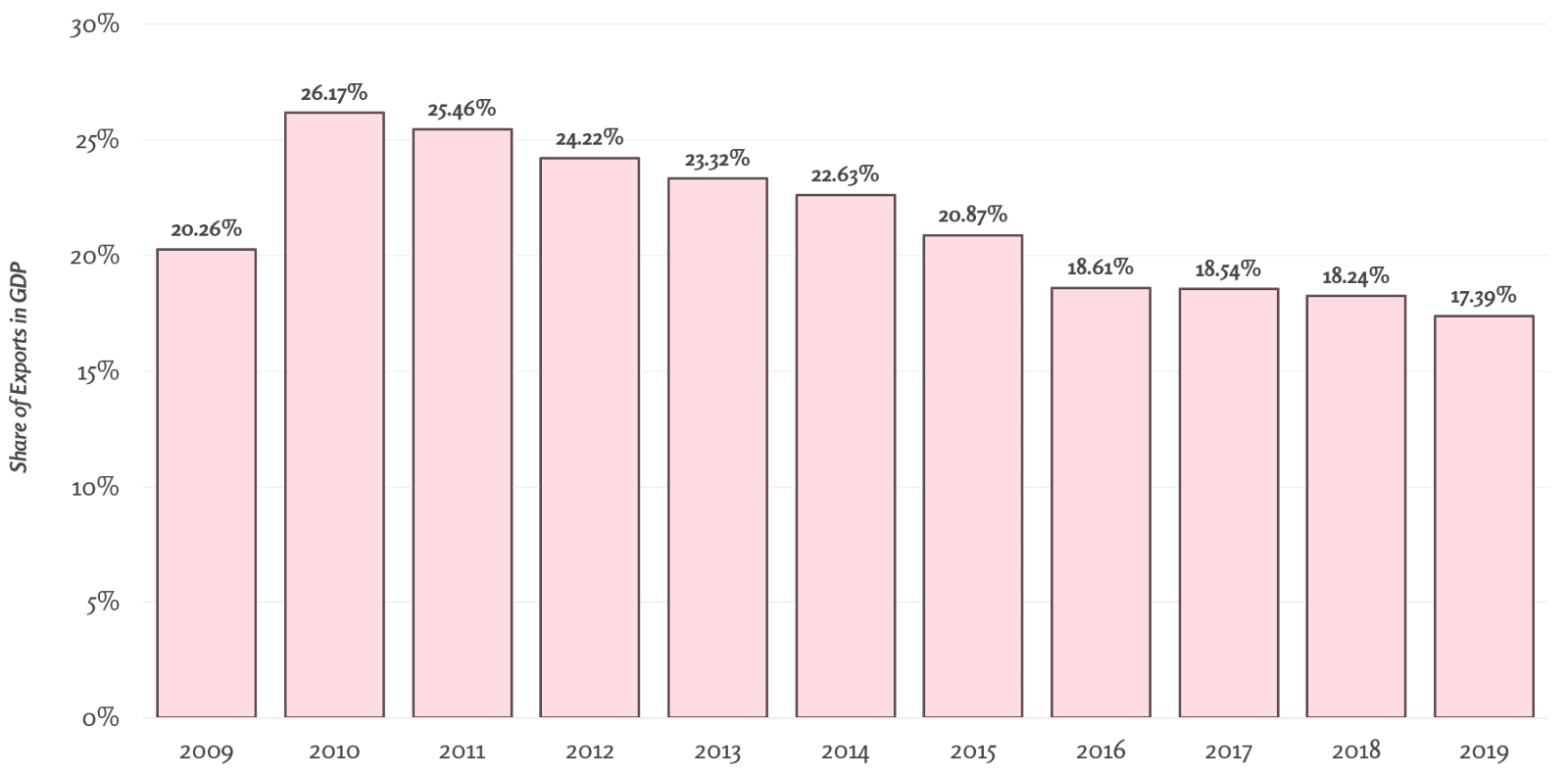

Due to fundamental differences in political and economic policy, China has found itself in a teetering position. Recent estimates of export reliance show that exports make up approximately 17% of China’s total GDP, and as such, these strained relationships have pushed Beijing to place additional value on two FTAs: the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (TPP11) and the Regional Comprehensive Economic Partnership (RCEP).

China Exports as a Percent of GDP

New FTAs for Shifting Priorities

To minimize the economic impact of rapidly deteriorating trade relations, China is using the TP11 and the RCEP to bolster its import-export industries. Many experts have questioned the country’s decision to participate in both, as there are many duplicate member states in both treaties.

Countries Participating in the RCEP and the TPP11

RCEP vs. TPP11

China is a current member of the RCEP, a proposed trade agreement with 15 other countries. The other participating nations combined account for 30% of the world’s population and just under 30% of the world’s GDP.

The RCEP is seen as a very inclusive deal by many countries and has looser standards on labor issues, environmental protections, and dispute resolutions. The RCEP has the potential to be the largest FTA in the world, with participating RCEP member states comprising an approximate combined GDP of US$21.3 trillion and 40% of global trade.

TPP11, by contrast, is a smaller agreement with only eleven member states. Still, the TPP11 packs a punch: the trading bloc currently represents 495 million consumers and spans 13.5% of total global GDP. The US was slated to participate in the TPP, the TPP11’s predecessor, but pulled out shortly after President Trump’s election. The US’ absence has created a vacuum that has created an opening for China to dramatically increase its role in global leadership.

As a result, much of the previous regulatory governance within the deal became less stringent without the US’ support. For example, the US had been the driving force behind the ability for companies to sue national governments as well as the ability for copyrights to be extended 70 years past an author’s lifetime in the original TPP, though both proposed regulations ultimately lost support after the US’ withdrawal.

It is important to note that these two agreements are not mutually exclusive. China will reap more rewards by participating in both FTAs without having to choose one over the other as both partnerships offer distinct key benefits. The RCEP offers China a unique opportunity to both bolster trade with high growth countries while also establishing standards and regulations for the trade bloc. At the same time, the TPP11 may allow China to strengthen trade relationships with countries that it has historically been underexposed to.

Why RCEP?

The RCEP seeks to reduce tariffs amongst members. While Beijing currently holds longstanding free trade agreements with many of the proposed RCEP member states, including the Japan-China-Republic of Korea FTA and China-ASEAN FTA, further reducing barriers through the RCEP comes at an opportune time as trade with ASEAN partners like Vietnam and Thailand alone are up 18.1% and 9.2%, respectively, in the first half of 2020. Despite already enjoying organically growing trade figures, reduced barriers and expanded industry access via the RCEP will only serve to strengthen trade relationships going forward.

More importantly, China has set its scope on increasing its trade influence by setting standards in the RCEP deal. China’s increasingly China-first trade policies are the common denominator behind China’s failing trade relationships with the West. From lagging environmental regulation to intellectual property protections, China has relied on policies set forth through its system of “socialism with Chinese characteristics” to maintain economic growth.

It has become abundantly clear, however, that its values and norms strongly contrast with those of the West. As the brainchild of China, the RCEP lends China the unique opportunity to set the tone on regional regulatory policy, thereby granting Beijing the chance to exert influence in the region. The RCEP lacks the same chapters on environment regulations and labor standards as are included in the TPP11, while the deal also strategically avoids discussing state-owned enterprises – a cornerstone of China’s economy. All in all, the deal skimped on many areas of regulation, with the 20-page agreement 14 pages shorter than its TPP11 counterpart.

Why TPP11?

It is still widely speculated whether China will join the TPP11 as it rebuilds relations through other FTAs. The TPP11 is stronger on free trade, and joining it would expand China’s economic allies around the world while signaling that the country is serious about reform and opening up. Additionally, with the mandated elimination of virtually 100% of tariffs on manufactured goods (one of China’s largest industries), the TPP11 would encourage further trade and investment into the country – delivering both tangible and intangible benefits to the Chinese economy.

China Underrepresented in Americas’ Trade

Furthermore, the TPP11 may offer China a strategic inroad to increase trade with the Americas, a bloc with which China has had comparatively lower engagement. China has historically imported much more than it has exported from Latin-America, and liberalized trade could offer an opportunity to build more balanced relationships. Chinese-Chilean trade is one such example; after the two nations signed an FTA in 2006, bilateral trade from 2006 and 2018 grew by 345%.

Mexico has already expressed interest towards a bilateral trade agreement with China and sees the value in a trade deal with China. Mexico has long been a strategic target for increased Chinese trade presence, and a multilateral deal through the TPP11 could be one of such ways to accomplish this, while simultaneously expanding Chinese trade influence to other member nations. Overall, the TPP11 would offer China an opportunity to tap into new global markets as opposed to simply bolstering regional trade within Asia.

Looking Forward

Although negotiations have stalled in recent years, China has expressed its commitment to finalizing the RCEP agreement by the end of 2020. Most of the original participants have expressed a firm commitment to the agreement amid increased pressure from the pandemic to finalize and ratify the deal.

China’s participation in the TPP11 deal is much more speculative, however. The deal would require vast amounts of domestic reform within the Chinese market, including increased oversight of labor, environmental, and intellectual property regulations, which would negate some of the benefits of the RCEP deal.

Furthermore, the new US-Mexico Canada Agreement (USMCA) enacted a clause in which any party may review other FTAs under consideration by a member nation and decide to leave the USMCA should any agreement be signed with a ‘non-market’ economy. This puts strain on China, as Mexico or Canada could be incentivized to retract its TPP11 membership upon China’s confirmation. Still, despite these concerns, Premier Li Keqiang affirmed the country’s interest in the deal at the National People’s Congress in May.

The combined influence across the global market that China could gain from the TPP11 and RCEP is undeniable. By removing nearly all tariffs on traded goods and increasing influence with countries outside of Asia, China would be able to not only maintain, but also potentially forge new relationships with key trade partners. Long term, China’s participation could boost external confidence in its economy while supporting its domestic export industry for years to come. Overall, how these deals play out over the remainder of 2020 will be a hot topic to watch.

Pingback: TWS: July 30 - August 6, 2020 | The China Guys

Pingback: The RCEP: A Big Deal Unlikely to Resolve Sino-Australian Disputes | The China Guys