Healthy living has always played an important role in Chinese society. Whether partaking in taiqi or evening walks, Chinese culture has long emphasized a balanced lifestyle. As the Chinese middle class has expanded to approximately 350 million people, more consumers have been empowered to further invest in their bodies and wellbeing. This new movement depicts a bright and competitive future for China’s health and wellness industry.

While gyms and fitness centers are becoming popular in major cities such as Shanghai and Beijing, the industry is still in infancy in smaller cities and rural areas. Therefore, vitamins and dietary supplements present an accessible alternative for those still wanting to participate in the wellness movement. The internet has become the local pharmacy, delivering many of these products to millions of WeChat and Weibo users. Foreign brands, mostly from Australia and the United States, maintain a high reputation and offer solutions that speak to the Chinese market, maintaining their competitiveness against local brands. As a result, local brands aim to gain an edge in other ways, including localized advertising, low-price leadership, and superior customer service.

China’s Changing Attitude Towards Healthy Living

Despite its relatively recent appearance within the Chinese economy, China’s healthy living industry is quickly gaining in popularity. The country appears to be embracing a wide variety of health solutions, whether that be due to government support, heightened awareness, or changing beauty standards.

In 2017, a study determined that only 50% of Chinese adults met the WHO’s daily recommended amount of vegetable and fruit consumption. This was attributed to low socio-economic status and poor health literacy. The Chinese government has confronted this head-on by passing a series of legislation related to nutritional education, with these policies aiming to increase nutritional intake in vulnerable populations by increasing nutritional literacy and encouraging healthy eating habits.

In addition to governmental support, studies have found that healthy living has generally become a key priority for younger generations. A 2019 survey found that both Millenial and Gen-Z consumers placed a higher emphasis on “living a healthy lifestyle” than finding love or being financially successful.

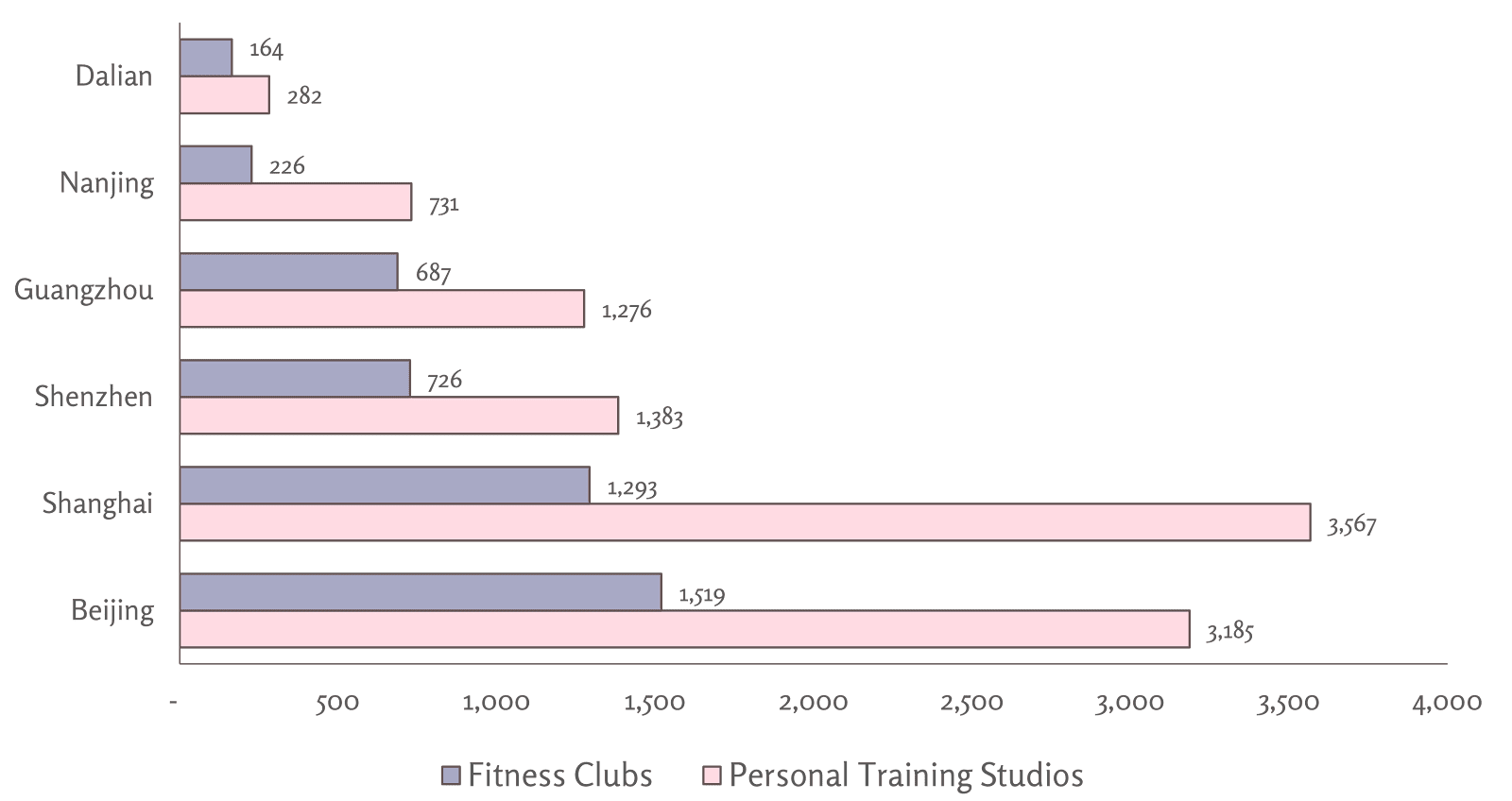

With significant interest towards healthy living, major Chinese cities and urban centers are seeing a transformation. Gyms popping up in Beijing, Shanghai, and other major hubs indicate a growing trend towards increased exercise as shown by the emergence of supporting facilities. Beijing and Shanghai, for example, have nearly 10,000 personal training centers and fitness clubs among them, though China’s second- and third-tier cities are lagging behind. Nanjing and Dalian, two second-tiered cities with respective populations of eight and five million, have only a combined 1,400 fitness centers.

Exercise Facilities Begin to Pop Up in Major Chinese Cities

Complementing a healthy diet and exercise, vitamins are a natural supplement to a holistic approach to health. The Chinese population’s top health concerns relate to skincare, sleep, anxiety, and hair loss, all which stem from unique cultural traits of the nation. Chinese beauty standards fuel a broad spectrum of vitamin needs, such as Vitamin C and Vitamin A ointments which are commonly found in skincare products. Vitamins that target anxiety also see high levels of adoption by the younger Chinese demographic who may be seeking a convenient solution to counter a highly competitive professional, academic, and familial environment. Overall, the average Chinese consumer is eager to experiment with natural remedies while vitamin and dietary supplement companies capitalize on the emerging industry via targeted and creative marketing methods.

The pandemic has further increased demand for health supplements. According to the Baidu Index, COVID-19 has led to an increased interest in immune system strength and bodily health, which has boosted vitamin supplement sales and led to increased discussion of health and lifestyle choices by the Chinese media. This increased interest is mostly led by 20-29 year-olds, with 57% of interest in vitamins stemming from Chinese women.

Foreign Brands Cash In on Their Luxury Status

As consumers become more interested in their health and are willing to invest more in their bodies, many are willing to pay a premium for what are perceived as higher quality foreign brands’ products. In fact, some of the most sought after products are nutritional supplements from Australia. In 2019, Australia accounted for 22.3% of all health food and supplement imports into the Chinese market, beating the USA for the top spot. Australian brands such as Swisse, Cenovis, and Blackmores have been instrumental in solidifying the country’s dominance within the industry. Beyond Australia, other major foreign brands, such as Centrum from the US, Jamieson from Canada, and Fancl from Japan, have all captured significant market share in China.

While foreign competitors all have slightly different approaches to the Chinese market, most have a common avenue: cross-border platforms. Due to misleading, or even occasionally toxic, products, the Chinese government began placing tight restrictions on dietary supplement companies between 2005-10. The extreme bureaucracy and resources required to apply for such permissions made establishing a physical brand in China extremely difficult; therefore, companies turned to e-commerce platforms such as Tmall, WeChat, JD Worldwide, and Koala as their primary sales channels to keep their physical presence overseas while still being eligible to sell to the Chinese market – albeit with significantly lower barriers to entry.

Though cross-border e-commerce platforms have allowed foreign brands to break into the Chinese market, significant success can also be attributed to online branding campaigns. WeChat, Weibo, and Douyin have all become critical marketing avenues for foreign brands, wherein consumers are able to read, review, and share promotional content. Most foreign brands have also found success in localizing their marketing efforts, connecting with target consumers through shared values, tasteful slogans, local modeling, and even partnering with China’s live streaming influencers. Clinicians, a New-Zealand based supplements brand, is a prime example after the company realized a 40% rise in sales after beginning to host live streaming sales sessions on Tmall Global with several key opinion leaders.

While most foreign brands focus on targeted advertisements from the comfort of their overseas locations, some notable brands have cut through the red tape to establish physical presences in China. GNC, a US brand, had long opted to own and maintain a storefront presence across China; however, after a lengthy and costly battle within the fiercely competitive retail market, the company recently made the decision to sell its Chinese operations to Harbin Pharmaceutical Group after declaring bankruptcy in 2019 with Q1 2020 net losses surpassing US$200 million. Just as many other rapidly developing industries in China, China’s health and wellness brands have begun to feel the pressure to keep up with digital developments within the marketplace in a bid to innovate or die.

Local Brands Take the Top Spot in Price Leadership

While foreign brands are considered to be the more luxurious of the dietary supplements, domestic competitors have also built a reputable repertoire. Brands such as By-Health, Conba, and Yangshengtang have built trustworthy names and their products and message are well aligned with the Chinese market.

Local brands in China’s health and wellness industry pride themselves on their product presentation and curb appeal. By-Health, for example, has established a strong user base and positive reviews. On Tmall, one of the brand’s beauty-focused vitamin products has 4.9 stars across almost 34,000 reviews, with many testimonials applauding the vitamin’s taste and ‘cute’ packaging. The company’s focus on ‘cute’ branding and ‘handsome’ models has resonated well with its target market, as one review claimed, “the pink and tender packaging satisfies my girl’s heart and I like it very much. I tried two [vitamins] as soon as it arrived and [they] tasted good. I’ll keep taking them.”

An additional advantage that Chinese firms are able to leverage is their reasonable prices. By producing domestically, Chinese firms are quite often able to beat their foreign competitors by keeping their prices under CN¥100. A 2020 survey showed that 55% of all health supplement purchases were made for under CN¥100, although the price range for certain retailers extended well beyond CN¥300. A key challenge to foreign brands’ pricing models is a 13% postal tax that accompanies cross-border shipping, which is in addition to a 9.1% general tax on health and wellness products. Though foreign brands are typically perceived as more luxurious, price leadership has given local brands an additional foothold in the industry.

Other Healthy Living Trends

While vitamins and dietary supplements have enjoyed significant traction by Chinese consumers, the lifestyle trend towards a healthy lifestyle extends beyond popping pills. Many consumers are also opting for a more active, involved approach to their health that includes more nutritious eating and increased exercise.

These two areas have been more challenging for foreign brands to tap into. Decathlon, Nike, and Adidas are foreign brands that have been locked in a fierce competition with the likes of domestic brand Li-Ning to bring more workout-based and fitness-related products to China. Decathlon, a French outdoor brand, first came to China in 2003 and appealed to customers in major cities through its targeted ad campaigns. Their stores are filled with sporting and outdoor gear of every kind, and even come complete with an indoor play area filled with bikes, skateboards, and scooters to provide an engaging consumer experience. The brand has seen moderate success in China, though its operations are largely contained to the larger first- and second-tiered cities.

Beyond Meat is also attempting to capitalize on Chinese cultural emphasis on healthy eating as a means of building strength. The company has paired with Starbucks to bring, “simple, plant-based ingredients without GMOs, soy or gluten.” Beyond Meat will also begin to manufacture some of its products out of Shanghai, which will further set the stage to market meat-alternative products to a health-conscious Chinese audience.

Looking Forward

Whether through foreign or locally-branded products, China’s middle class has begun investing in their own health. The pandemic will continue to consolidate interest in the emerging health and wellness industry that has maintained an average annual growth of 10% for the past 7 years and reached a market size of CN¥222.7 billion in 2019. Despite pandemic-related economic toils, the industry is one of the few that is still expected to see continued growth in 2020, with both foreign and domestic brands well poised to reap the rewards of their efforts in an increasingly competitive and digitized business environment.

Pingback: TWS: Oct. 19-26, 2020 | The China Guys

Pingback: Looking Past Luxury in a Post-Pandemic China | The China Guys