Critics of the “One Belt, One Road” initiative tend to conflate China’s lending practices, asset seizure, and debt distress in a way that makes China out to be the villain of the OBOR story. But, in reality, the devil lies in the details. China’s lending practices are often not predatory in nature; instead, most cases show debt forgiveness accompanied by additional lending as opposed to asset seizures. Still, while Beijing’s original intention may not be to bend its partners to its will, the viability of various projects is questionable to say the least. Many projects along the Belt and the Road are riddled with corruption, poor logistics, and bad financial management. In this article, we will look at two particular OBOR development projects, namely Kenya’s Standard Gauge Railway and the Hambantota port in Sri Lanka, and unravel the true cost of funding these projects.

Kenya

Kenya’s Standard Gauge Railway (SGR) is a marquee OBOR project in Africa. At the China-Africa summit in 2020, President Xi Jinping highlighted the critical role played by the SGR in delivering essential goods to the landlocked nations neighboring Kenya during the coronavirus pandemic. Currently, construction is on hold with the railway tracks ending abruptly 75 miles west of the Kenyan capital of Nairobi. Once completed, the SGR would connect Kenya’s port city of Mombasa with East and Central African countries.

The SGR was constructed at a high price of US$3.3 billion, but funding required to extend the line from Nairobi to Uganda has not been forthcoming. As alarm over Kenya’s financial health has raised questions regarding the viability of the project, allegations of debt diplomacy have tarnished China’s reputation locally as well as in the international community.

Did the railway line make financial sense?

Due to the crumbling state of infrastructure among the nations of Eastern Africa, intra-trade is severely restricted. Connecting the major cities via railways would reduce transportation time and costs, thereby boosting trade and exports via the Mombasa port. But at US$5.6 million per kilometre for the track alone, Kenya’s line cost close to three times the international standard and four times the original estimate due to the difficult terrain upon which the track was built.

To service the loans taken for construction, the fares charged for transporting goods along the SGR are exorbitant. It costs about US$800 to truck a container from Mombasa to Nairobi, but it costs US$1,100 by rail. The lower demand for freight resulted in revenue of US$126 million in 2019, falling greatly short of the operating cost, which was estimated to be US$170 million. Hidden operating costs, high interest rates, and a closed bidding process all result in a reduction of the project’s overall profitability.

There is also the question of ample supply. A 2013 World Bank study predicted that freight traffic on the entire East Africa Community rail network would grow to approximately 14.4 million tonnes per year by 2030. The same study found that investment in a standard gauge railway appeared “only to be justified if the new infrastructure could attract additional rail freight in the order of 20-55 million tonnes per year.” By that measure, the railway would need to win all of the freight currently trucked to and from Mombasa and more to make fiscal sense.

What if Kenya fails to pay the SGR loan?

It is rumored that, if Kenya fails to repay the loans for construction advanced by Chinese lenders, it risks losing the lucrative Mombasa port. Terms of the loan specify that the port’s assets are collateral, and they are not protected by Kenya’s sovereign immunity due to a waiver in the contract.

This is not a new concept, as ratings agency Moody’s has warned:

Countries rich in natural resources, like Angola, Zambia, and Republic of the Congo, or with strategically important infrastructure, like ports or railways such as Kenya, are most vulnerable to the risk of losing control over important assets in negotiations with Chinese creditors.

If there is a probability of China seizing Mombasa port then why does Kenya borrow from Beijing?

Middle income countries such as Kenya face a major hurdle in raising capital for infrastructure investment. International institutions such as the International Monetary Fund (IMF) and World Bank place conditions on loan disbursements which have positive long-term effects but can cause short term pains. The IMF policy, namely the structural adjustment program, promotes austerity measures such as cutting government borrowing and spending, lowering taxes and import tariffs, raising interest rates, and privatising state owned enterprises. Since Kenya’s membership in 1964, it has had 19 such arrangements with the IMF. With more than half the population living below the poverty line, these austerity measures have led to a poor standard of living, high unemployment as well as corporate failures. Even though the IMF offers below-market interest rate loans, given these conditions, African nations are turning East for their development finance needs.

China is miles ahead of the IMF and World Bank when it comes to funding for Africa. Since the turn of the 21st century, China has funded 1,076 projects in Africa amounting to US$148 billion, making Africa one of the biggest recipients of Chinese investment. With Africa being a critical source of raw materials for manufacturing, Beijing’s growth is intrinsically linked to Africa and thus the relationship is symbiotic, where one cannot thrive without the other.

Over the past decade, Beijing has written off US$3.4 billion and restructured or refinanced about US$15 billion of African debt without seizing assets from borrowers. Further evidence of China’s largess can be found from instances of debt renegotiations with neighboring Ethiopia. The Addis-Djibouti standard gauge railway has similar characteristics with the Kenyan SGR. Ethiopia, China’s second-largest African borrower, received a cancellation on all interest-free loans up to the end of 2018. This was on top of the previous renegotiated extensions of major commercial railway loans agreed earlier in 2018. In other words, the way China handled debt repayments with Ethiopia and other countries in Africa may set precedent for Kenya in its renegotiations with China.

Sri Lanka

Politicians often associate debt-trap diplomacy with Hambantota, a small port town in Sri Lanka. The town has received numerous substantial investments from the Chinese government, and the Sri Lankan government has struggled to stay on top of its payments. However, this analysis discounts crucial details regarding the Sri Lankan government’s flagrant mismanagement of debt and overly attributes their debt crisis to Beijing. To get a more in-depth understanding of the matter, we must first look at Sri Lanka’s debt load and the port separately.

Relations between China and Sri Lanka

China has been the largest arms supplier of Sri Lanka since the 1950s. Under guidance from the Sri Lankan President Rajapaksa, defence and security cooperation between the two countries intensified during the Sri Lankan civil war. During this period, he relied on China for economic and military support.

President Rajapaksa is credited with ending the civil war in 2009, albeit with a devastating record of human rights abuses. From that point onward, the President and his family controlled ~80% of all government spending, making them culpable for the financial situation of Sri Lanka.

The port built in the President’s home district is viewed as a vanity project. With space to expand the thriving port in Colombo, there was no demand to construct another port. Lenders such as India refused to fund the project, questioning the necessity for a second. Along with the port came an international airport and a cricket stadium with Chinese contractors and the Rajapaksa name.

The Hambantota port opened with an elaborate celebration on Nov. 18, 2010. Two years later, the port only drew in 34 ships during the whole of 2012. Construction costs soared as port expansions continued only to fulfil Mr Rajapaksa’s dream. Corruption along with wasteful projects resulted in Sri Lanka’s debt increasing threefold within 10 years. In sum, Hambantota’s main challenge came from within Sri Lanka itself. In 2017, unable to service its debt obligations, the Sri Lankan government sold a controlling equity stake in the port and 15,000 acres of land around it for 99 years for US$1.12 billion.

Was the port a debt trap from the start?

To examine whether the port was a debt trap we have to understand Colombo’s checkered history. Prior to its close ties with China, Sri Lanka suffered from balance of payment (BOP) crises at regular intervals since 1965. As a reflection of the depth of the crises, it has had 16 arrangements with the IMF. Colombo has a budget deficit problem combined with a trade deficit. The first is due to wasteful public expenditure far surpassing the country’s revenue, and the second is because imports exceed exports, thereby creating a shortfall of foreign exchange. With dwindling foreign reserves, Sri Lanka has struggled to pay back its loans to international creditors.

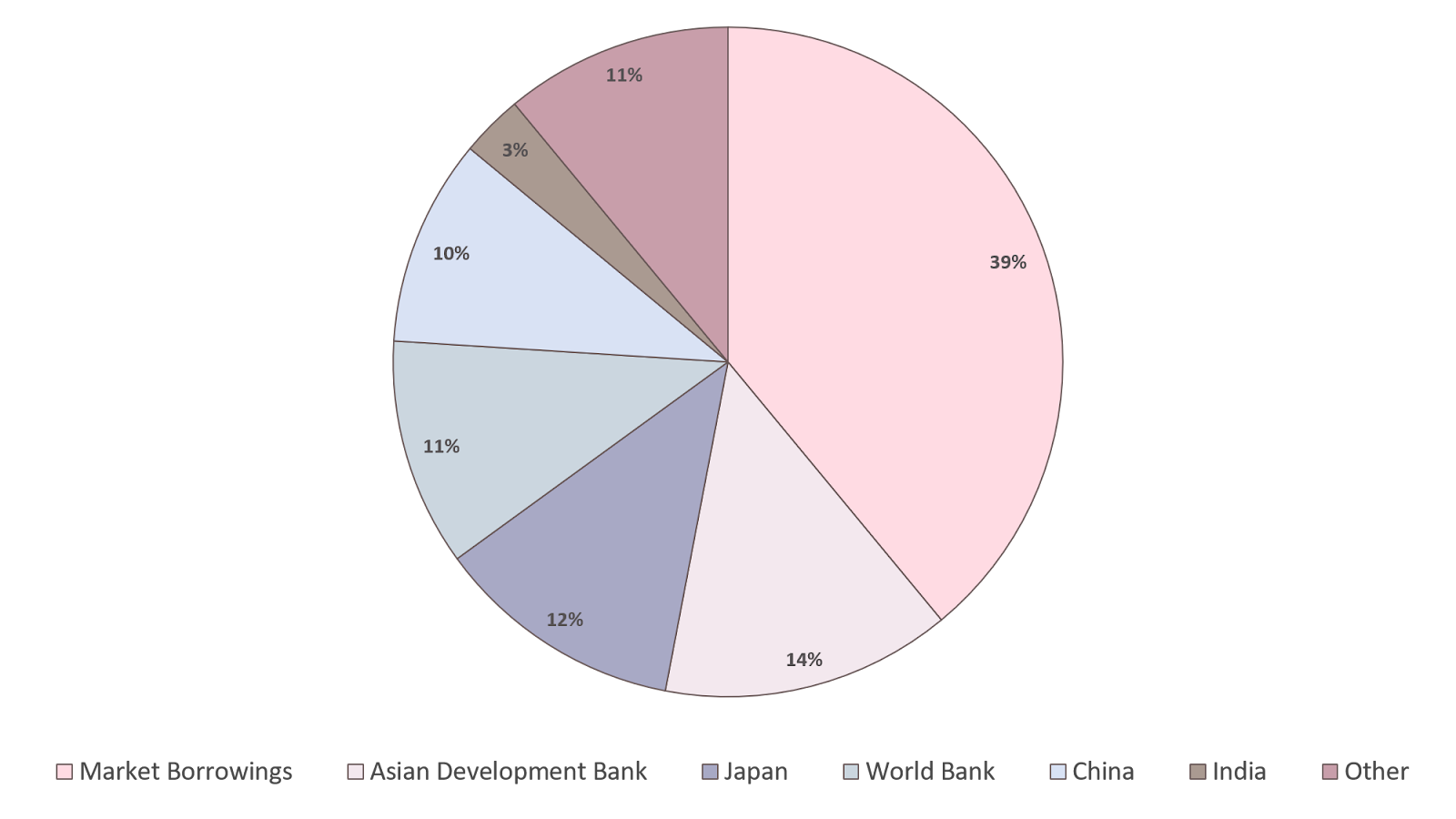

Sri Lankan Debt Stock by Lender (2017)

A breakup of Sri Lanka’s creditor composition shows that the largest portion of foreign debt are commercial borrowings raised in international capital markets. China holds 10% of Colombo’s foreign debt, behind commercial borrowings, ADB, Japan and the World Bank.

Commercial loans charge a higher interest rate (6-7%) as compared to concessionary loans (2-3%). Two thirds of the Chinese funded Hambantota loans were at a fixed rate of 2%, with a five year grace period, while one early loan for the first phase, at US$307 million, was at a fixed rate of 6.3%. These rates were far lower than Sri Lanka’s commercial borrowings from bond markets.

In 2016, Sri Lanka’s foreign exchange earnings from exports were insufficient to meet its international debt obligations. The country’s foreign reserves, which were US$8.34 billion in July of 2019, are becoming increasingly stretched, and the government will have to find US$17 billion to pay for maturing foreign loans and debt servicing between 2019 and 2023.

To avoid the twin troubles of facing another balance of payment crises and not having enough reserves to pay its international creditors on time, the port was sold. Further evidence of the country’s need for cash is that the money from the sale of the port was used to strengthen the country’s foreign exchange reserves, not to reduce the country’s high level of debt.

Fast Forward to 2020

Sri Lanka must make US$4.8 billion in debt repayments in 2020. The coronavirus pandemic has dwindled Sri Lanka’s foreign reserves to US$7.2 billion as of April 2020. The China Development Bank has agreed to a financing facility of US$500 million to help tide the country as they control the coronavirus pandemic.

Even though the country faces constraints with servicing its loans, cabinet ministers have approved a decision to borrow US$80 million to improve 105km of roads. Unchecked borrowing like this will force Sri Lanka to face another BOP crisis. Unless the debt burden is reduced and the twin troubles of budget and trade deficit under control Sri Lanka will be in continuous need of emergency financing.

Looking Forward

Kenya and Sri Lanka are under debt distress, but the blame should not be exclusively placed on China. Feasibility studies complimented with disciplined debt management controls – both items that these countries lacked – are needed for developing countries to avoid falling into debt. For Kenya, the outlook that China will be open to debt renegotiation is high; the precedent for this has been set in the past by many other cases on the continent. As for Sri Lanka, the nation was not prepared to take on such a project in the beginning, and a sale of assets was the only feasible outcome.

While these two cases serve to disprove the notion of debt diplomacy, it has to be said that assessing the borrowing credibility of nations is a responsibility that falls on China’s shoulders. With the pandemic making the financial situation of developing countries worse and as the “One Belt, One Road” initiative continues to expand, China needs to reassess its opportunistic lending tactics for the future.

Aditi Taswala is a guest contributor to The China Guys and authors the newsletter: Filtered Kapi.

Pingback: TWS: Sept. 28, 2020 | The China Guys