As technological advances are made in the smartphone and telecommunication industries, companies and countries both have recognized the growing importance of semiconductor chips. These tiny electronic devices, smaller than a postage stamp, act as the data-processing brain for a range of products from smartphones to computers. Without the use of semiconductor chips or integrated circuits (ICs), personal devices would not be able to store data and function efficiently.

Given the importance of these chips to modern technologies, semiconductor technology has become a flashpoint in US-China relations as the two superpowers struggle for technological dominance. In 2020, Washington levied a series of sanctions against Huawei and similar Chinese companies to limit Beijing’s access to leading semiconductor technology. These US Treasury Department sanctions restricted the export and transfer of US-made semiconductor technology as well as prevented the sale of foreign made chips developed or produced from US software and technology.

Without access to US-made semiconductor technology or foreign chips of comparable quality, Chinese tech companies will struggle to sustain the production of higher-end products and expand internationally. In light of US sanctions and foreign competition, Beijing has unveiled economic incentives to encourage innovation in the domestic semiconductor industry. These incentives, including the exemption of corporate income tax for up to ten years, are designed to accelerate R&D expenditure and consolidate semiconductor production within China’s most advanced chip fabrication plants or “foundries.” As Washington threatens to impose further economic sanctions in its war of attrition against Chinese tech companies, Beijing is racing to modernize its domestic chip production capabilities before the technological gap grows larger.

China’s Look Inward

In a time before great power rivalry defined US-China relations, namely the late 1970s, Beijing sought to modernize the country’s domestic semiconductor industry with Washington’s support. However, Cold War tensions and a deep mistrust for communist countries gave rise to strict US export controls, which prohibited shipping the most advanced technology to China. Recognizing US assistance would not come in the form of diplomatic technology transfer agreements, Beijing launched two IC foundries in early 2000: Grace and SMIC. To supplement the growth of these new enterprises, Beijing lured established market competitors, Intel and Samsung, into the domestic Chinese market with the promise of low labor costs and a skilled workforce.

The price of admission for these companies and many others was forced technology transfer (FTT), an economic policy Beijing continues to use to date to coerce foreign businesses to share their technology and trade secrets in exchange for market access. Without stating the obvious, China’s strategy to attract foreign business through diplomacy and financial incentives was a masterstroke fueled by US economic interests and Beijing’s shrewd trade policies. However, semiconductor technology within the US, Taiwan, and South Korea continued to outpace China and the country has been forced to rely on foreign chipmakers.

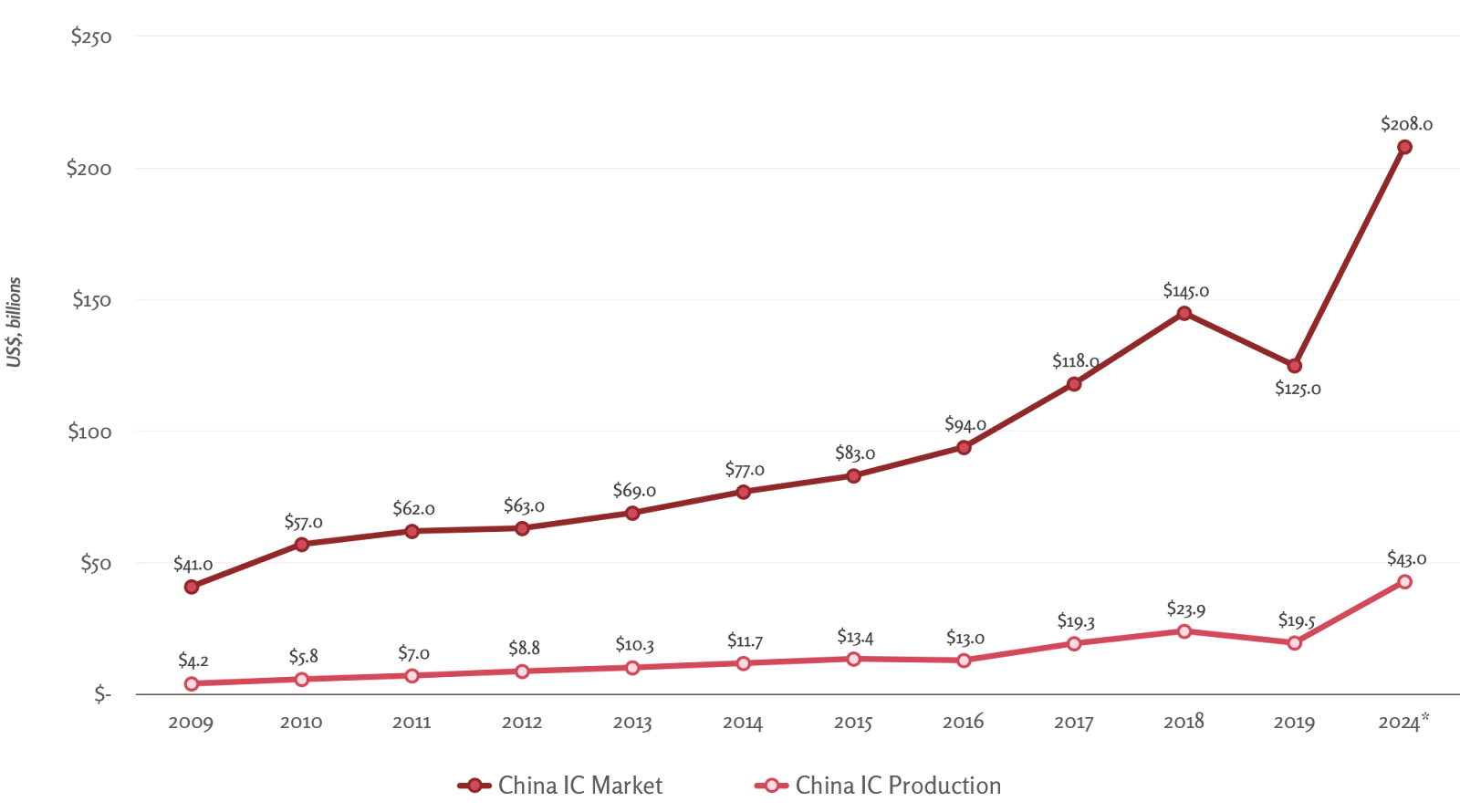

In 2014, China consumed US$77 billion worth of chips; however, only 15.1% of those chips were manufactured domestically. To address the concern that China had failed to establish itself as a major player within the tech industry, Beijing launched in 2015 “Made in China 2025,” an economic initiative to increase the domestic production and research of critical emerging technologies, including semiconductor chips. The Chinese government set an audacious target to produce 70% of the semiconductors it uses by 2025. As seen within the exhibit below, China is unlikely to reach its production targets and is projected to manufacture 20% or US$43 billion of the US$208 billion IC market in 2025.

Gap Between Domestic Production and Market Demand for Chips Projected to Grow

This shortfall, which can be attributed to multiple factors, including a lack of technical talent, a less innovative domestic business environment, and the previously mentioned US economic sanctions, has been noted by Beijing. To overcome these obstacles, the government has pushed an economic policy of zìzhǔ chuàngxīn or “indigenious innovation” to promote the development of Chinese semiconductor technology.

On August 4, 2020, the Policies of Promoting High-quality Development of Integrated Circuit Industry and Software Industry was released to address the concerns within Beijing’s ruling party. This policy, which is devised to accelerate the design and production of more advanced semiconductor nodes, offers a wide range of tax breaks, favorable financing, and talent development for leading IC software and manufacturing enterprises in China. The exemption of corporate income tax (CIT) for up to 10 years, access to Beijing’s “Big Fund,” and collaboration with students from leading universities illustrates the ruling party’s commitment to pursuing a turbocharged strategy of technological growth in the face of US sanctions. While China is still in need of foreign direct investment and higher-end semiconductor technologies, leading Chinese firms are starting to take advantage of Beijing’s generosity.

China’s Shift to Local Sources

One of the hardest hit companies in the US-China semiconductor conflict is Huawei. Due to Washington’s sanctions, the Chinese tech giant cannot source higher-end materials from traditional suppliers TSMC and Samsung and must rely upon leading domestic firms SMIC and Huahong.

As these local companies lack the technological expertise and EUV lithography machinery to design and produce the most advanced chips, 7nm nodes, Beijing has encouraged public and private investment to meet short-term demand and to build products and solutions for the future. The party also wants to aid the development of top-tier design firms, including Cambricon Technologies and Unisoc, to ensure China’s IC industry continues to innovate and grow. Although these initiatives promise long-term transformation, local sources may struggle to fill the backlog of chip orders for Huawei and others in the near-term.

SMIC

The largest advanced foundry in Mainland China checks all of the party’s boxes: 2019 revenues of US$3 billion, listed on the STAR Market of the SSE, and incorporated in the Cayman Islands as a limited liability. Beijing’s Big Fund has taken notice of SMIC’s dominant market position and injected US$2.2 billion in Q2 2020 to provide access to additional cash flow as the firm expands its operations. This increase in working capital coupled with the SMIC’s US$6.6 billion offering on the STAR in Q3 has built a war chest that could be used to build new semiconductor foundries, create competitive R&D programs, and ultimately help the firm challenge global rivals TSMC and Samsung.

In the short-term, however, SMIC will struggle to satisfy the needs of Huawei and other firms searching for domestic alternatives to higher-end IC technology. Given SMIC has the capability to only manufacture 14nm nodes, which trails in comparison to the state-of-the-art 7nm nodes produced out of Taiwan and South Korea, Huawei has built a 2-year reserve of essential chips to shield its operations from US sanctions. SMIC will also likely face US export controls if added to the US Department of Treasury’s “Entity List,” representing a further obstacle to the company’s supply chain and ability to develop its technology to meet the requirements of domestic firms. Without further insight into what Washington will do next and the future advancements of SMIC, it is unclear how the company will serve as the primary source of higher-end IC technology in China.

Huahong

As the twin sister of SMIC, Huahong is the leading manufacturer of semiconductor wafers in China. The company’s revenues and HKSE market cap of US$1 billion and US$29 billion in 2019 suggest it has the size and stamina to meet domestic needs for semiconductor chips. However, Huahong also lacks the technical prowess of leading IC firms TSMC and Samsung, and would only be able to provide low-tech chips to Huawei and others. In comparison to SMIC, Huahong has not received any notable investments from the Big Fund or other private sector sources in 2020. This lack of financing raises the question whether Huahong is even considered an important player within Beijing’s grand strategy of semiconductor dominance. With the looming threat of US sanctions against SMIC, Huahong may be able to absorb its competitor’s lost capacity. However, it is equally difficult to predict the firm’s long-term success during this difficult geopolitical environment. From the current trajectory, it appears that Huahong will continue to operate in the current market space as a low-to-mid tier chip manufacturer.

Semiconductor Design

Cambricon Technologies / Unisoc

Domestic IC design is another core consideration in Beijing’s strategy to reduce China’s dependence on foreign technology. Without encouraging domestic innovation, China will be unable to compete with ROC and ROK-based firms. Cambricon Technologies and Unisoc are two companies within the design sphere which stand to benefit the most from Beijing’s economic policies.

Cambricon Technologies is a rising star in the IC design industry and is considered the most valuable artificial intelligence chip designer in China. The Company’s Q3 2020 IPO on the STAR for US$369 million outlines the company’s ambitions to raise capital and expand operations within China. As a former major supplier of Huawei’s first AI chip-powered smartphones, Cambricon has the brand name recognition and experience to compete within the domestic marketplace and create higher-end technology. Even with the uncertainty surrounding China’s semiconductor industry, Cambricon is in position to capitalize on the ruling party’s economic policies and potentially rival foreign competitors in the future.

Unisoc, a chip design unit of Tsinghua Unigroup, could also fill the void in the domestic marketplace if US sanctions are placed on SMIC and Huahong. The company’s expertise in the global baseband market is vital to producing IC processors for 5G smartphones and tablets. Beijing has recognized the brand’s importance and extended US$635 million from China’s Big Fund, a clear indication government insiders believe in the long-term success of the company. If Unisoc can continue to obtain external financing and compete with other baseband firms, the firm will be an important source of home-grown IP that other foundries can rely upon.

Looking Forward

Washington’s economic sanctions represent a significant obstacle to Chinese technological independence. Without access to leading semiconductor chips and technology, Huawei and other firms are being forced to stockpile high-end technology and look-inward for resources that aren’t readily available. Beijing’s recent economic policies of tax incentives and state-backed financing will be essential to maintaining growth within an industry which is being constricted by the increasingly combative US-China rivalry. Several large enterprises, including SMIC, Huahong, Cambricon Technologies, and Unisoc could stabilize production within China and ensure the industry’s future success. However, it is clear Huawei and these Chinese companies will struggle in the short-term as the lack of access to supplies inhibits the design and production of semiconductor chips.

Pingback: TWS: Sept. 14-21, 2020 | The China Guys

Pingback: Upgrading the “World’s Factory” Through China's Fourteenth Five-Year Plan | The China Guys

Pingback: China Chips Away at Taiwan’s Semiconductor Talent Pool