While promoting an internationalized renminbi over recent years, China has cautiously juggled the three facets of the “impossible trinity,” while slowly relinquishing control of its capital account and “managed float” currency regime. However, global adoption of the fledgling currency has lagged due to the country’s unwillingness to fully liberalize capital flow.

China holds the second largest economy in the world and accounts for over 40% of international trade, yet as of May 2020, only 1.79% of global payments have been conducted through the RMB. The US dollar’s international dominance, China’s hesitancy to move decisively towards one side of the “impossible trinity,” and illiquidity of offshore RMB have dampened international attitudes towards the currency. In response, Beijing has sought to combat US dollar dominance and replenish offshore liquidity through its “One Belt, One Road” initiative, a large-scale overseas infrastructure program. Through ‘attractive’ loan packages, China is making new friends in lesser-developed regions and attempting to form an early network of RMB users.

Regardless, trade deficits and net outflows of RMB amongst trade partners continue to pose a risk of offshore illiquidity that threatens China’s grand strategy. To combat this, China began signing bilateral swap agreements (“BSA”) with nearly anyone and everyone that showed interest. Currently, China has agreements exceeding US$500 billion across 35 countries – more than any other country by a wide margin – that provide RMB liquidity to trade partners with drying markets to boost trade over the long-term. To date, swap options have gone largely untapped, which is likely a product of muted foreign interest in the renminbi; however, slow upticks in global RMB adoptions could see swaps used by an increasing amount.

What are BSAs?

A bilateral swap agreement, or cross-currency swap agreement, gives a recipient party the right to exchange currencies with a counterparty at a fixed interest rate. BSAs are often used to both reduce the risk of currency fluctuations in times of financial volatility as well as a tool with which to lubricate cross-border trade. Countries with open capital flows are exposed to liquidity risks when their financial obligations exceed the amount of currency a country can acquire while swap agreements allow trade activity to proceed by using a given currency to replenish foreign exchange reserves and fulfill the debt obligation, all while mitigating the risk of loss through currency exchange fluctuations. At their core, BSAs function as a line of credit between global currencies.

Whereas BSAs have historically been signed to safeguard against liquidity crunches, Beijing has approached the tool with a different goal – currency internationalization. In target markets like Pakistan, China hopes to support RMB-denominated trade by recycling currency. As Pakistan maintains a trade deficit with China, Pakistani exporters spend more renminbi than importers receive, which depletes the country’s RMB reserves. Over time, this will ultimately reduce opportunities for additional RMB adoption due to illiquidity in the market. In theory, should Pakistan be properly incentivized to continue using the RMB for cross-border trade, Pakistan’s central bank could tap its line of RMB credit to exchange Pakistani rupees with the People’s Bank of China for RMB at an interest rate pre-determined by the swap agreement.

China’s Swaps in Action

Within the last 10 years, China has entered into BSAs with an astounding 35 countries – 21 more than the US with the second-highest number of currency swap partners at 14. Despite numerous agreements and more than CN¥3 trillion available for swaps, very few countries have actually drawn upon their credit lines. While China’s ambitions have materialized into signed agreements, the BSAs have been more symbolic than anything, with little indication that the agreements have increased RMB use abroad. Furthermore, most instances in which countries have tapped into their BSA were initiated due to a lack of alternative options rather than a desire to onboard RMB.

Use Cases: RMB as an intermediary

Pakistan and Argentina are two of the few nations that have tapped into their BSAs, though not in the traditional sense. During times of financial crisis, both Pakistan and Argentina have used the agreements to obtain RMB and convert it into USD in offshore markets.

Pakistan was the first country to do so when it tapped into its US$10 billion line in 2013 after seeing a sharp dip in its foreign reserves. Rather than using the liquidity to bolster RMB-denominated trade with China, however, it exchanged it for USD to shore up its reserve cache.

A similar situation ensued in Argentina in 2014. As the nation faced extreme inflation of the peso and teetered on the brink of an economic crisis, it was unable to obtain US dollars, inhibiting importers from purchasing vital consumer goods. Argentina drew upon its BSA with China, but like Pakistan, rather than using it to facilitate trade between the two countries, the RMB was instead part of a two-pronged approach by Argentina to introduce USD into its domestic economy. In both instances, China did not protest against the RMB being converted to USD, rather emphasized how the agreements could bolster international trade between the nations.

By providing liquidity during times of crisis, China has proven to be a reliable partner. The reputation may have begun to pay dividends, as the Sino-Pakistani BSA doubled from CN¥10 billion (US$1.42b) to CN¥20 billion (US$2.84b) in 2018 and Pakistani trade settlement in RMB surged by 250% in 2019. As recent as March 2020, Pakistan proposed that it be further increased to CN¥40 billion (US$5.68b). Similarly, Argentina increased its currency swap agreement with China from CN¥70 billion (US$9.94b) to CN¥130 billion (US$18.47b) in 2018. These deals represent the progress being made on RMB internationalization and the potential for bilateral trade to expand in the future as China remains a strong and dependable financial partner.

Use Cases: ‘De-dollarization’

In another instance of BSA utilization, Russia drew upon its swap agreement between October 2015 and March 2016. Though undisclosed how much was actually exchanged, a press release from the Russian central bank noted that the funds were allocated to a limited number of Russian and Chinese counterparts for the purpose of ‘supporting bilateral trade and direct investment between the two countries.’ As such, trade experts have suggested that the RMB did ultimately make its way to Russian companies and that the funds were used in trade with China, leading to increased settlement between the two countries.

However, like both Argentina and Pakistan, this deal may simply have been a targeted hedging move. Russia drew upon the BSA as western sanctions caused the ruble to fall sharply. When drawing from Chinese BSAs, Russia was able to subvert US-imposed sanctions as sanctions largely target operations that use USD – when Russian transactions were conducted in an alternative currency, they were able to bypass any restrictions. Therefore, the purported increase in Chinese and Russian trade was ostensibly driven by Russia’s intent to employ a strategy of “de-dollarization,” or US sanctions avoidance as opposed to reasons relating to the RMB’s value as an international currency.

Use Cases: Liquidity

In mid-June of 2020, Turkey engaged in a swap with China. The US$1.7 billion BSA between the two countries represented approximately 8% of the total US$21.08 billion of trade value between the two nations in 2019. Following a government attempt to prop up the Turkish lira, Turkey had desperately depleted its foreign exchange reserves and sought help from financiers like the IMF and the US. Unable to secure critical funding, Turkey pivoted to China for assistance via its swap agreement.

According to the Turkish central bank, while the move was economically motivated, the influx of RMB ultimately drove increased RMB-denominated trade settlement. Additionally, there are ongoing discussions of expanding the line of credit between the two countries in order to help Turkey circumvent a major currency crisis, which will likely scale RMB integration within the Turkish economy.

Reality of Agreements

In reality, these are only a few isolated cases in which swap agreements have actually been drawn upon. Of China’s 35 BSAs, very few have been effective in facilitating trade between China and its trade partners. The agreements certainly boost China’s diplomatic influence as a short-term bank of intermediate liquidity when Western institutions are unavailable; however, very little impact on trade has materialized.

Variables with Impact on Chinese Trade

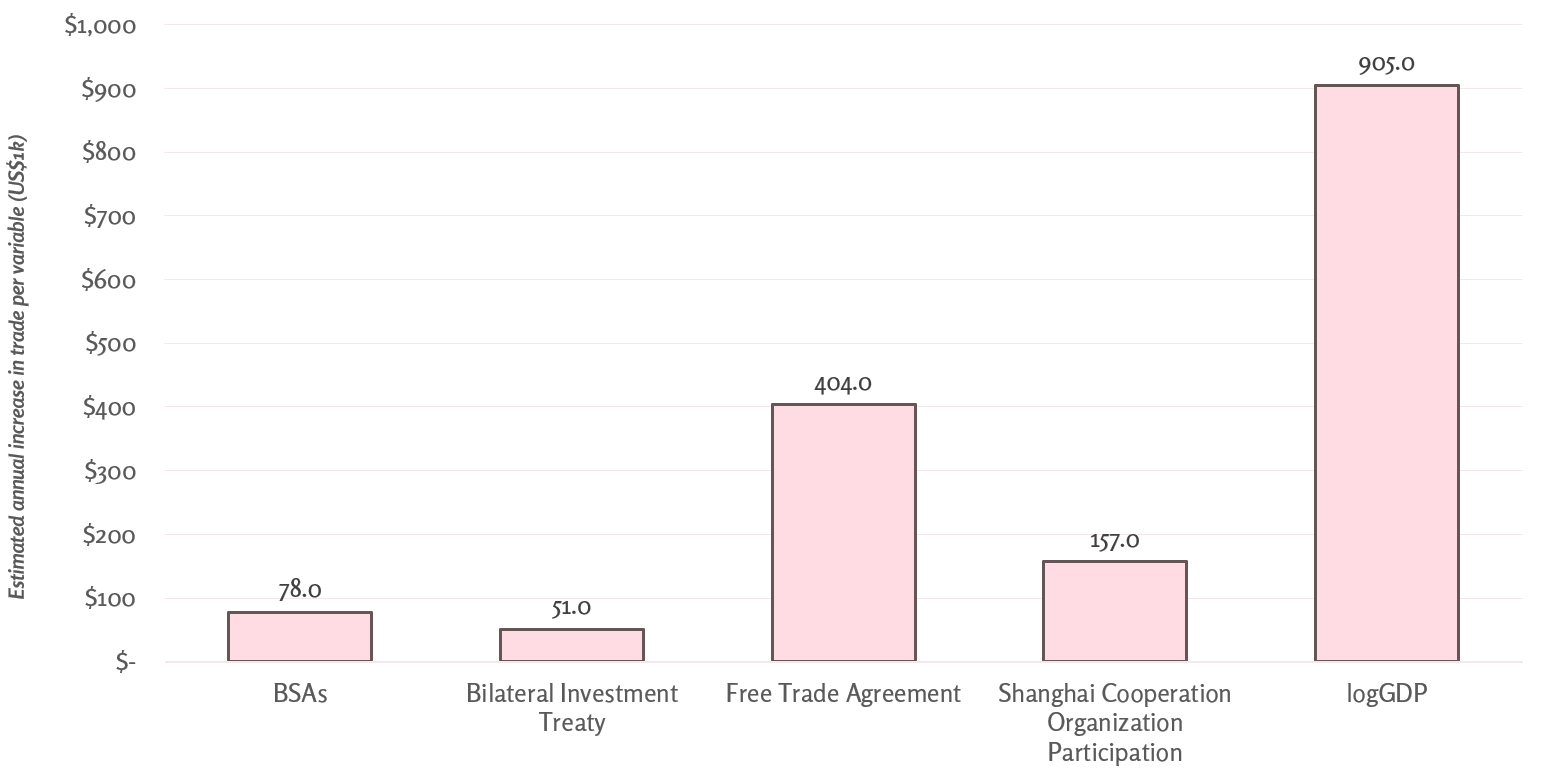

To analyze the efficiency of BSAs in meeting China’s overarching goal, we ran a regression analysis on different various factors and their correlation to trade activity. The model demonstrates the correlation between a one unit increase in the independent variable in relation to a US$xx.xx increase in annual bilateral trade. Through the above results, it can be observed that while having a free trade agreement (FTA) or a higher GDP may correlate to larger increases in bilateral trade, bilateral swap agreements hold comparatively negligible influence. The coefficient for BSAs points to an average annual trade increase of US$78,000 per signing of a BSA, while a one point increase in logGDP presents an estimated $900,000 annual bonus in trade. US$78,000 is but a mere blip in the context of China’s total trade, implying that BSAs are failing to achieve one of their main objectives: boosting bilateral trade.

Until China fully opens up its capital accounts and bolsters international support for RMB use, it is unlikely that BSA partners will have much incentive to tap into their swaps; but, if China;s RMB internationalization goals are realized, BSAs are likely to exert a much stronger impact on trade.

Looking Forward

So far, China’s BSAs have failed to materially drive the internationalization of the RMB. While many agreements are in place, the RMB lacks a robust framework for countries to value it more highly than the USD or Euro. In most of the instances in which BSAs were drawn upon, the RMB was simply leveraged as an intermediary to obtain USD and generated minimal traction in increased RMB-denominated trade.

That said, there is value in the BSAs. The US$500 billion total available through China’s BSAs represents a potential catalyst for increased trade activity between China and its trade partners in the future. Additionally, China’s ability to offer an alternative channel for liquidity outside of the Western financial system is welding diplomatic relationships that will serve to increase global confidence in the RMB. As China slowly phases out capital controls, RMB usage is likely to slowly grow, and BSAs may play an increasingly important role in the sustainable offshore circulation of the redback over the long-term.

Pingback: TWS: July 2 - 9, 2020 | The China Guys