As the novel coronavirus emerged, mandatory government-enforced quarantine measures resulted in the closures of factories, shops, and corporations alike, and consumers curtailed spending to prepare for hard times. Ever since, both developing and advanced economies have been colored red by recession characterized by widespread layoffs and plunging stock markets. In June 2020, The World Bank forecasted that the global GDP would contract by -5.2% or more over the course of the year.

Despite being positioned as the original epicenter of the coronavirus pandemic and bearing harsh first quarter results, China has managed to quickly contain the spread of the virus and reinvigorate its economy. The nation led its striking turnaround by implementing strong anti-virus containment measures and providing well-targeted fiscal and policy-based stimulus, which heralded stark results. In the second quarter, China became the first major economy to produce year-over-year growth in a quarter; in the third quarter, China was the first to reach composite annual growth in 2020.

Nonetheless, not everything that glitters is gold. Behind the growth figures, China’s economic dynamics were extremely off-balanced. In quarters two and three, fiscal stimulus and material stockpiling played defining roles as the primary economic drivers, while consumption, China’s bread and butter of growth, remained muted. However, each quarter since has shown improved results, and rising figures for income, consumption, and foreign investment are painting a positive outlook for the fourth quarter and beyond.

Looking Back at China’s Mid-2020 Results

Lopsided Growth in Q2

Following China’s first economic contraction since Mao Zedong held office, China’s 3.2% GDP growth in Q2 surprised economists, who had forecasted growth around the 2% mark. While growth is growth nonetheless, the drivers behind China’s GDP pointed to lopsided growth. Departing from precedent, China’s largest driver of growth, household consumption, had fallen flat in Q2. This powerhouse segment typically contributes around 40% of China’s GDP in a good year, yet at the end of Q2, consumption remained in negative territory.

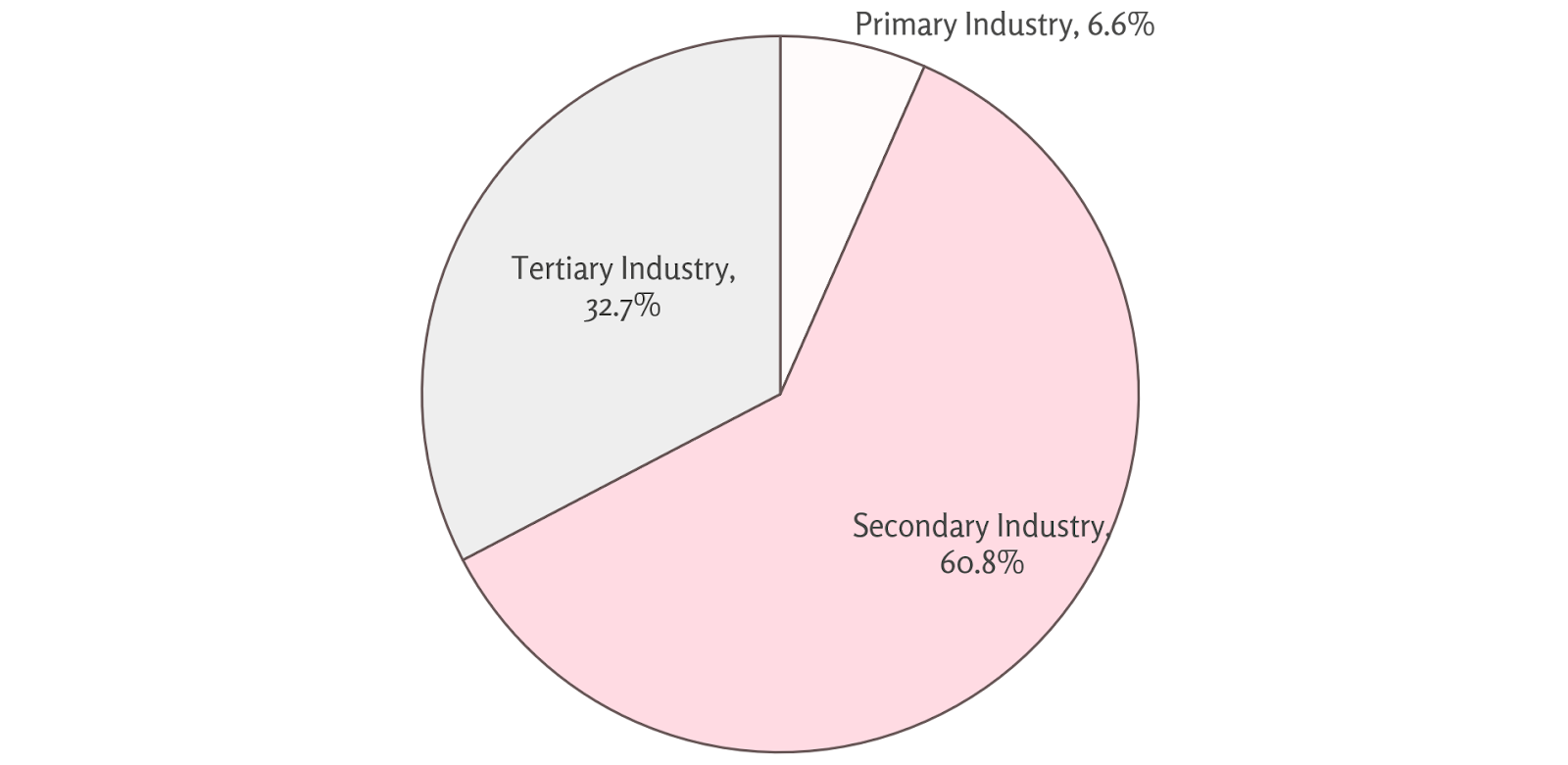

So, if not from its traditional source, then where did China’s growth come from this year? At the GDP component level, the key driver was gross fixed capital formation (“GFCF”), another term for fixed asset investment. Before explaining GFCF in depth, it helps to understand the sector level breakdown. Secondary industry – construction, industry, and manufacturing – soared at 60.8% of GDP growth in Q2. Primary industry, or agriculture, contributed 6.6%, and tertiary industry, or services, lagged at 32.7%.

Secondary Industry Drives Economic Gains in Q2

While a boost to secondary industry performance could normally be attributed to heavy manufacturing sales, Q2 consumer spending figures indicated otherwise as retail sales remained down -10%. Production continued to climb across intermediary products like steel and iron, yet consumption of end products – take automobiles for example – was muted, pointing to a lopsided market wherein production was booming but end sales were nearly nonexistent. Gross fixed capital formation in the construction industry and material stockpiling in the manufacturing industry were the culprits behind the difference.

Gross Fixed Capital Formation (GFCF)

GFCF covers new investment into fixed assets like buildings, equipment, and infrastructure. This component of growth comprised a whopping 156% of China’s Q2 GDP, while consumption weighed on growth at -73%.

Driving the growth in GCFC was China’s central fiscal stimulus, of which half flowed downwards to support provincial and local level infrastructure projects. In May, Premier Li Keqiang announced CN¥1 trillion in additional federal spending raised through special quota bonds, as well as CN¥1.6 trillion worth of special bond issuances at the provincial and local level. This funding served primarily to invest in infrastructure projects, which provided significant support to China’s secondary industry. For example, investment in physical infrastructure like railways and roads rebounded quickly, and both broke into positive accumulated growth at 5.7% and 2.4% respectively in July.

Infrastructure Shines Among Shadowed Investment in Q2

Construction firms added to the macro-economy by way of capital formation in infrastructure projects, and industrial firms benefited through the provision of materials to support these projects. In addition, most analysts reached the consensus that there must have been significant material stockpiling during the quarter due to a stark discrepancy between rising industrial production levels and muted manufacturing and retail sales. The auto industry was a prime example. Metals production continued to rise as auto sales slumped, which resulted in average backlogs of vehicles at China’s dealerships jumping from a 45-day supply to a 444-day supply.

Overall, China’s second quarter growth painted a picture of an economy growing on shaky legs. The role of stimulus in development was markedly apparent, leading to investors’ concerns over the sustainability of development due to the finite nature of fiscal stimulus. While growth is generally a positive result, Beijing and global investors alike prefer sustainable, organic growth led by consumption and private investment. 3Q 2020’s figures fell more in line with these expectations as they illuminated an economy largely driven by organic growth.

Q3 Activity Gains Steam

China’s economy as a whole grew by 4.9% in Q3, bringing 2020 aggregate growth into positive territory at 0.7%. Not only did the new quarterly figures surpass those of Q2, but they were also more closely aligned with pre-pandemic compositions. The three components of GDP growth – final consumption, GFCF, and imports/exports – contributed to growth at 34.9%, 52%, and 13.1%, respectively. While trade remained stable, consumption saw enormous gains from its -73% contraction while GFCF dropped to more normal levels from its 156% gains in Q2.

Sector-level contributions mirrored this growth as well. Final consumption is a major factor for tertiary industry – services and retail – which saw its share of growth reach 45.4%, up from 32.7% in Q2, while secondary industry’s contribution dropped to 47.7% from 60.8%. Albeit slightly more industrial-centric, Q3 growth was more closely aligned with pre-covid growth indicators (historically, China has supported its growing economy through consumption in retail and services) as rising consumption pushed tertiary industry upwards. A rebounding tertiary industry in Q3 was a welcomed shift as yields on fixed asset investment may vary but consumption leads to guaranteed economic returns.

Tertiary Industry Regains Its Footing in Q3

The positive upticks in consumption and retail sales may provide relief to Beijing, which has assumed a larger-than-usual budget deficit to dole out stimulus through both infrastructure spending and supportive measures for businesses. Though unlikely to occur in the final months of 2020, Chinese officials may begin to pull back on tax and social security exemptions as industries continue to regain their footing in early 2021 – assuming Q4 growth continues to normalize.

Looking Forward at China’s Economy in Q4 and Beyond

Trends in Income

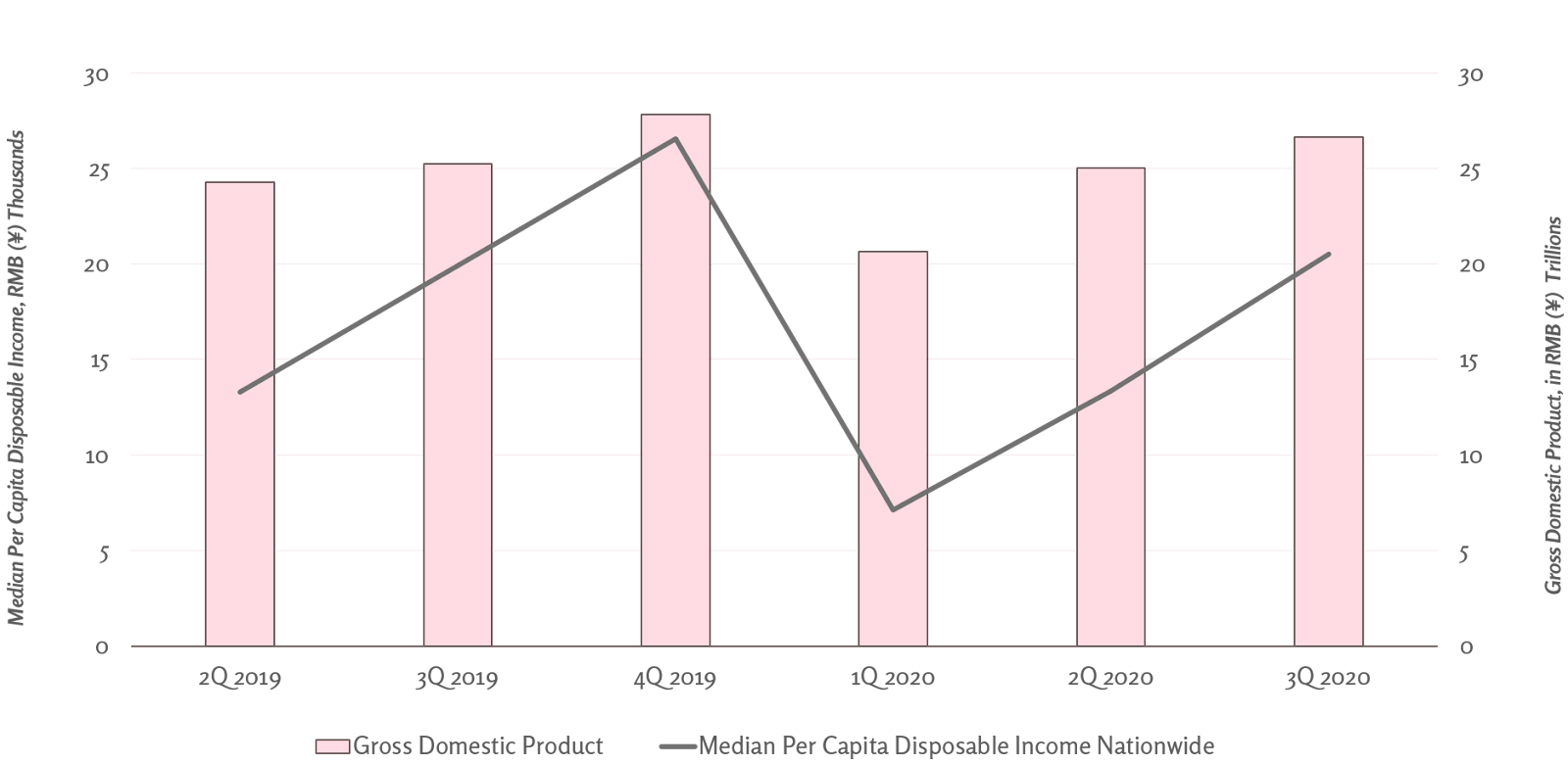

With two months left in 2020, the economic outlook for China’s Q4 and beyond is quite strong. Alongside the recent release of Q3 GDP data, the National Bureau of Statistics also released quarterly data on incomes. After falling off sharply, per capita disposable income nationwide grew by 0.6% year-over-year while median income grew by 3.2%, pointing to positive job and wage growth. While particular concerns have been placed on China’s lower wage earners who shouldered the hardest blow in the pandemic due to uneven distribution of stimulus relief, rural households that tend to be associated with low incomes saw average disposable incomes reach CN¥12,297 (US$1,852), or CN¥675 (US$102) higher than incomes at the same time last year.

China’s Median Incomes Recover Alongside GDP

This quick recovery was largely due to Beijing’s effective quarantine measures and policy-based stimulus. Despite being positioned as the original epicenter of the coronavirus, 99% of businesses had reportedly resumed normal operations by the end of March, just three months after the first cluster of cases of COVID-related pneumonia were confirmed in Wuhan. Since then, Beijing’s comparatively light-handed approach to economic stimulus was focused upon relieving businesses through cost-cutting measures, such as providing tax and social security contribution exemptions and lowering barriers to credit. By prioritizing resources towards the supply-side, businesses were able to retain more employees even as their doors shuttered during and following the mandatory quarantine, which ultimately facilitated a quicker economic reboot.

Trends in Employment

Despite its efforts, Beijing’s policy support still fell short. In the period following quarantine, troves of workers filed for unemployment. At the outbreak’s peak in February, China’s unemployment rate jumped from 5.3% to 6.2%; however, unemployment has since leveled at 5.4% as of September.

Nonetheless, given China’s notoriously opaque unemployment calculations, it is difficult to accurately assess to what heights domestic unemployment actually swelled. Poignantly, unemployment figures are based on surveys of urban employees, which overlooks the nation’s sizable rural migrant population. Additionally, as China saw its largest class of undergraduates graduate in a period of surging unemployment, Beijing implemented reforms that recategorized digital and other non-traditional jobs such as “live-streaming” or “gaming” as official employment. Although these jobs occasionally may generate income, opportunities to earn livable wages are few and far between. As such, Beijing’s initiatives to reclassify employment definitions may have served to further inflate employment figures.

While current employment figures could well be off their marks, a positive trend in real employment is apparent enough through rising consumption numbers, income data, and consumer confidence surveys. The nation’s quick return to growth has heralded new opportunities for returning urban employees and migrants workers, alike. Vulnerable populations still remain, China’s 8.74 million graduates in 2020 for example have an unemployment rate 4% higher than their classmates a year earlier; but, all in all, consumers entered 4Q with greater job security and the confidence to boost consumption to more normal levels.

Promising Capital Inflows

While the World Investment Report 2020 estimated that global foreign direct investment flows shrank by more than 40% in the first nine months of 2020, China’s FDI inflows had been steadily rising. By September, China had received more than CN¥700 billion worth of foreign investment, up 5.2% year-on-year.

By quickly containing the spread of the novel coronavirus and injecting stimulus to resume growth, China positioned itself well to attract foreign investment. Additionally, China has executed market reforms in 2020, including opening its mutual fund markets to 100% foreign ownership in April. Since the announcement, the China Securities Regulatory Commission (CSRC) has received applications from UBS Group, JPMorgan, Nomura, Goldman Sachs, and more requesting to operate their Chinese ventures as wholly-owned foreign entities, which would commit boosted investment in their China operations. Earlier in the year, China reduced its National Negative List’s restricted industries from 40 to 33, opening the door to more foreign participation – and accompanying foreign investment – in fields like air traffic control, smelting, nuclear fuel production, and radioactive minerals. While market reform in 2020 has been less progressive than in past years, in the backdrop of a struggling global economy, Beijing’s market activity has allowed for new capital inflows that have been reflected in the nation’s strong FDI figures.

Clear Waters & Blue Skies in 4Q and Beyond

2020 has challenged the global economy with near-unprecedented levels of systemic risk. While China took a heavy blow, the nation’s strong virus containment measures and well-targeted stimulus response has quickly brought its economy back from the brink. Q3 figures have pointed to a better balanced composition of organic growth while prospects for 4Q and beyond look even more promising. While it may be premature for Beijing to reign in economic support measures during the remainder of 2020, officials will likely re-evaluate their supportive positions in 2021. Rebounding consumption and investment, paired with incremental market reforms, hint to sustained foreign investment in China over the coming year – particularly if other major global economies continue to stagnate under the weight of the outbreak. All in all, China’s growth miracle seems to have plenty of road left to travel.

Pingback: TWS: Nov. 9, 2020 | The China Guys

Pingback: The Risk of China’s Premature Stimulus Rollbacks to the Global Economy

Pingback: CvT: All-Time High Exports Cause Concern in Beijing