Following China’s first economic downturn since Mao Zedong was in office amid the COVID-19 pandemic in early 2020, China managed to finish out the year as the only major economy to see positive growth. Pushing ahead into 2021 on the momentum of economic recovery, China saw impressive growth figures throughout the first half of the year. However, the optimistic media headlines that declared “record growth” and “steady recovery” have quickly turned sour as 2021 approaches its close.

Despite continued economic growth, a variety of financial risks have begun to weigh on a Chinese economy that is already burdened with weak household consumption. Throughout the year, China’s bigwig policymakers have been playing a prolonged game of “whack-a-mole” on a variety of financial risks: unprecedented flooding, surging commodity prices, COVID-19 outbreaks, power outages, and rising defaults. Each case has offered unique challenges; but, by and large, the impact that each has had on the economy has been relatively isolated. Therefore, each problem has been largely transitory and has been alleviated with policy support.

By contrast, the impact of China’s rising defaults has been more widespread. The issue first began as a small wave of defaults across local government financing vehicles (“LGFVs”), state-owned enterprises (“SOEs”), and property developers in late 2020 and early 2021. Since, over-corrective de-risking efforts by the Chinese government have contributed to a serious cash crunch across the broader property market. This, when paired with slowing consumption and a rollback in economic stimulus, has led to a slowing economy at risk of hitting a wall. Some headlines are already drawing parallels to the 2008 housing crash.

China’s Financial De-Risking Goes Awry

A Growing Hunger for Debt

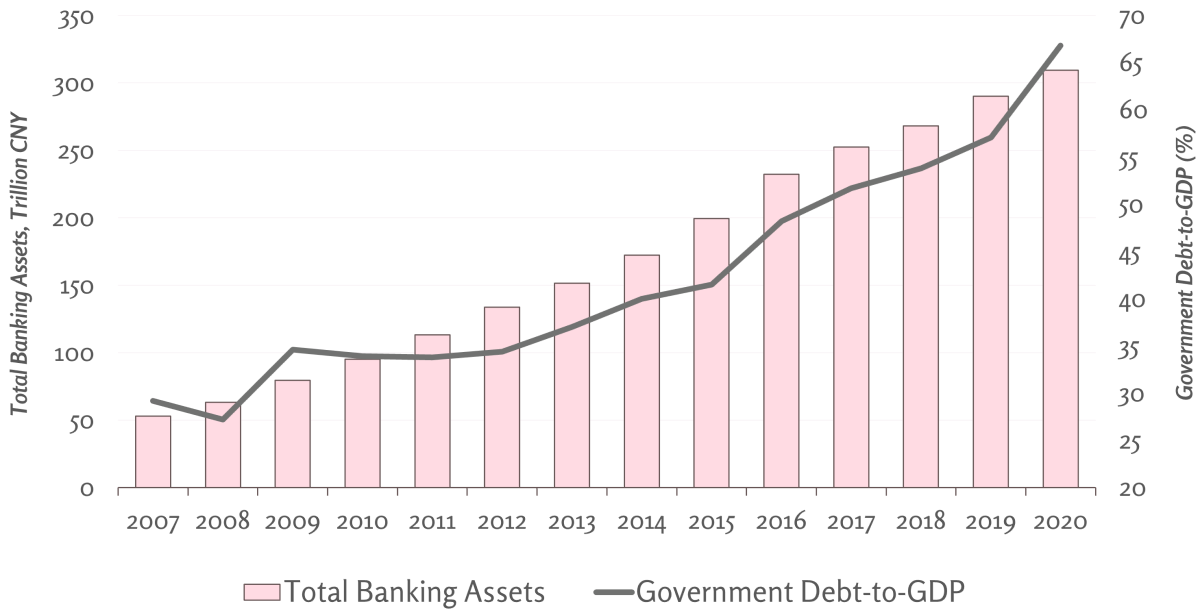

In the 21st century, China has charged forward with an unprecedented debt expansion. Following the 2008 financial crisis, Beijing worked with banks to support a struggling economy by providing accelerated lending. In 2009, banking assets grew by a whopping 25% year-over-year, marking a newfound thirst for borrowing. In the years that followed, credit growth continued to surge until the government put the brakes on bank lending in 2010. However, LGFVs began to soar in turn, with the most recent estimates pinning LGFV debt at US$7 trillion at the end of 2020. Debt has created a significant hangover problem for the Chinese economy, and some analysts claim the true levels of Chinese debt and nonperforming loans to be significantly higher than those shown by official statistics.

Rising Chinese Debt

The Chinese government, in response, unleashed a wide-scale financial de-risking and deleveraging campaign in 2015. Though, with the onset of the pandemic in 2020, an entirely new credit boom came into play. The government was left with no option but to temporarily shelve de-risking efforts as banks were encouraged to support struggling enterprises with relaxed lending. Loose monetary policy and heightened lending cultivated a favorable environment for credit access.

According to the People’s Bank of China, in January 2021, new aggregate financing, also known as social financing, reached CN¥5.17 trillion, or approximately US$810 billion. This marked a dramatic rise of 201% from the CN¥1.72 trillion in financing at the beginning of December 2020. While SMEs leveraged the credit to stave off bankruptcy, already heavily indebted industries also took this as an opportunity to line their pockets.

Financial De-Risking in the Pandemic

After navigating through its first economic contraction in decades, Beijing set to work on cooling the financial risks that had cropped up from overheated borrowing, particularly following notable defaults like that of Yongcheng Coal & Electricity Co. Instead of tightening lending on the broader economy through monetary policy, the People’s Bank of China advocated for a sector-by-sector approach to contain risk. While SOE debt was prominent, and the government conceded changes to its official policy stance in order to allow for SOE defaults, debt in the real estate sector was particularly worrying.

Beginning in October, against a backdrop of rising debt levels and rising housing prices, the government released a new policy known as the “three red lines” policy. The new policy seeks to slow credit growth among property developers and ensure sustainable growth within the industry. The “three red lines” place limits on debt-to-equity, debt-to-cash, and debt-to-assets growth levels, capping annual increases to no higher than 15%. Though originally intended to reduce risks by pushing developers to slowly relieve their balance sheets, the policy may have unintentionally created more risk, as developers failed to pull in enough revenue to pay their debts.

Challenges to China’s Housing Market in 2021

The Evergrande Bubble Pops

Since, debt and defaults have become a key theme in 2021, and 25 major Chinese businesses set a new record when they defaulted on US$10 billion worth of bonds before July. Amid tightening credit conditions, defaults like that of China Fortune Land grabbed headlines and spooked bond investors, though none have compared to the woes of the property behemoth, Evergrande Group.

With debts standing in excess of over US$300 billion, Evergrande is the world’s most indebted property developer. Despite the firm’s attempts to liquidate its assets — such as its infamous electric vehicles company — and the opportunity to reset some of its debt terms, the situation has quickly taken a turn for the worse. As of close of business on November 10, 2021, many investors still had not received an interest payment that was due after a 30-day grace period, potentially marking an official default and exacerbating China’s debt crisis.

China’s Policy Fix Worsens the Liquidity Crunch

The debt crunch is not limited to Evergrande, however. In recent developments, studies into China’s broader property market have found that more than two-thirds of China’s top 30 developers are breaching at least one of the limits set forth within the “three red lines” policy. Among which, a few particularly indebted developers with significant international exposure, such as China Railway Construction, are breaching two lines.

Unfortunately, China’s “whack-a-mole” approach to the risky property market has been rather unsuccessful at mitigating risks. Reduced lending during a pandemic, in which incomes from property sales had quickly dropped, exposed numerous developers to default risks as their cash coffers shrunk. The contagion has spread quickly: Kaisa Group, a Shenzhen-based property developer, suspended trading of its shares on Friday, November 5 in Hong Kong after the firm announced that it was faced “unprecedented pressure” on its finances.

Weak Q3 GDP Growth Compounds Woes

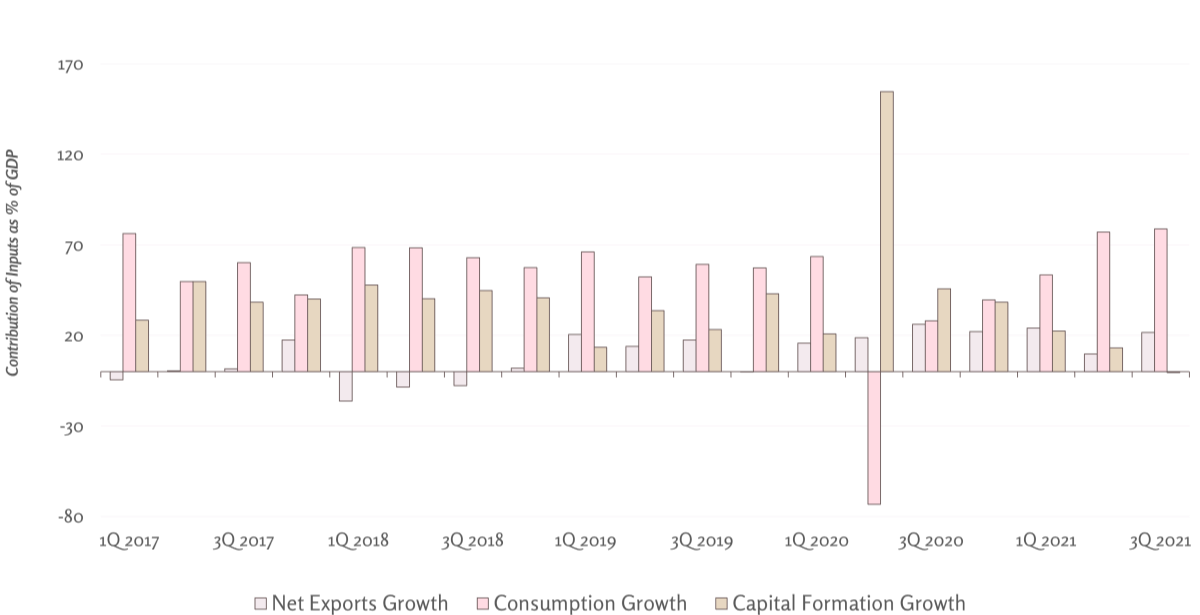

While the economy saw quick growth in the first two quarters of 2021, the government has failed to significantly stimulate consumer spending all the same. Alongside the rollback of stimulus and lending, lagging consumption has resulted in disappointing third quarter GDP figures. Clocking in at 4.9%, China’s 3Q GDP growth rate came in shy of the forecasted 5.2%. Quarter-over-quarter growth fell short of 3%.

Weakened GDP with the Rollback of Stimulus

With the rollback of stimulus, fixed asset investment has taken a backseat in economic growth, much in the hopes that consumption would take its place. These hopes have been misguided.

As of Sept 2021, year-to-date consumption has only grown 7% over the same period in pre-pandemic 2019. This is understandable though as it took two years to see the same growth in consumption that historically took one. Additionally, while consumption began 2021 with steaming momentum that saw Q1 2021 achieve 33.9% year-over-year growth, this was primarily due to muted consumption in early 2020 when China was still at the height of the pandemic. By the end of the second quarter, this low base effect had been lost and consumption growth slowed dramatically.

Slowed consumption only serves to magnify the looming property crisis and set the stage for a potential grand-scale ripple effect. Currently, more than three-quarters of household wealth in China is tied up in real estate, and Beijing has strong incentive to ensure that such wealth withstands a bursting property bubble. The collapse of Evergrande and other real estate developers would be detrimental to property values, which would deal a heavy blow to domestic wealth and lead to a further slowdown in consumption and investment. The results would be wide-reaching and devastating. All in all, strong forces are working to drag on China’s economic growth in the near future.

Looking Forward

In some ways, Beijing’s attempt to manage financial risks through deleveraging has backfired. Critics have called the government’s clampdowns too harsh and too sudden, as most major property developers have been left stranded without means to support operations through debt — a particularly perilous situation as businesses continue to shake the effects of the pandemic. The case of Evergrande and a slew of other heavily indebted property developers present a looming risk to the Chinese economy, and they particularly compound growing concerns over declining household consumption.

Additional defaults amongst property developers could send ripple effects that dramatically slow short-term economic activity while endangering long-term growth prospects. The Chinese economy is highly entangled with the property sector; some estimates suggest that as much as 29% of national GDP is generated by real estate production and property-related services. A struggling real estate sector could spell dire consequences for a variety of sectors, including LGFVs, construction, and banking and finance. Even the United States Federal Reserve has forewarned that China’s real estate sector poses risks to the US economy’s growth trajectory. As interconnected as China is to the global economy, it is best to keep your eyes fixed on the domestic property market to prepare for future events to unfold.